Due to COVID-19 and new restrictions being imposed on travel and large-scale public gatherings in the region, the Argus Media Added Value Fertilizer US Conference has been postponed. Dates for rescheduling are still being determined. Nothing is confirmed yet conference organizers are eyeing a mid-October date.

We will update this page as further details become available.

We’re very excited to announce that our Founder/Managing Director, Michael DeSa, will be participating as a panelist at the 4th Annual Argus Media Added Value Fertilizer Conference in Tampa, Florida from 10-12 June!

150+ delegates, new product trends and developments related to technology and sustainability in the added value fertilizer market.

As a largely subsistence farmer in northeast Texas and founder of an advisory firm servicing the global food and agtech sectors, Michael aims to add insight into the conversation around improving knowledge and know-how in the implementation of precision ag.

Investing in farmland has long been considered a viable and tangible alternative to paper markets, particularly for investors who lean toward the conservative end of the risk spectrum. However, finding an efficient and cost-effective way to profit from agriculture presents some challenges unique to the industry.

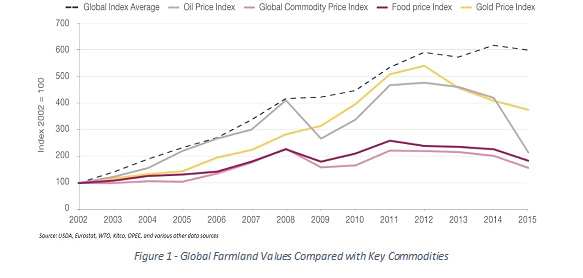

Owning farmland is the simplest and most direct way to invest in the agriculture industry. Agriculture has been an appreciating asset class for the last several decades. A Global Farmland Index developed by Savills World Research is comprised of data from 15 key farmland markets around the world. The index highlights an average annualized growth of 13.3% since 2002. Despite its strong return potential, nearly every acre of arable land in the country has either been converted for other purposes or is already in use as active farmland, making that acreage even more valuable. By 2030, urban expansion is projected to reduce global cropland by as much as 35 Mha (35 million hectares, or 74 million acres). Further, the cropland that will be lost is nearly twice as productive as the remaining land worldwide. In addition to the appreciation of the land itself, investors realize gains from the sale of crops harvested on their property.

Despite the clearly positive long-term investment potential of owning farmland, there are challenges to direct land ownership that cannot be ignored. Entering the agriculture industry in this fashion requires a large capital commitment that is beyond the means of the average investor. The time and expense of operating a farm are also often substantial, making ownership unrealistic for many. For these same reasons, investors who own farmland may struggle with liquidity when the decision is made to sell. Finally, direct farmland ownership comes with increased exposure to the cyclicality of commodity prices as well as operational risk.

Fortunately, a number of legitimate investment options exist for investors wishing to gain exposure to the agricultural sector in a way that doesn’t require titled ownership or operational management.

Alternative Agriculture Investment Vehicles

Land Lease Agreements

For investors who already own farmland, leasing property to another company or family willing to operate the land is an attractive opportunity. Operational risk can be transferred to the leasee and depending on how the lease is structured, property owners can benefit not only from predictable monthly lease payments, but also additional revenue generated from the sale of crops harvested from the leased land. For US farmland, attractive cap rates range between 3-5%. While incentives for the leasee to care for or improve the land long-term are limited, and the terms of operational control between the landowner and operator can be difficult to negotiate, it is a viable alternative for existing landowners wanting to reduce their operational risk and/or time commitments.

Real Estate Investment Trusts (REITs)

Investing in a REIT with exposure to the agriculture industry is another viable option. In 1971, US-based REITs had a total market cap of only $1.5 billion. At the end of 2017, the total market cap of all REITs listed on the New York Stock Exchange was $956 billion, a 63,633% increase. Currently, there are approximately 87 million Americans (44%of households in the US) who own REITs. Agriculturally-focused REITs typically purchase farmland then lease it to back to operators. REITs provide greater diversification than buying a single farm as they expose an investor to multiple assets across a wide geography. They offer greater liquidity than physical ownership, trading on many of the major stock exchanges, and can be purchased at prices much lower than acres of land. When it comes to agriculture REITs, two names dominate the space: Gladstone Land Corporation (LAND) and Farmland Partners (FPI). LAND was formed in 2013 and was the first publicly-traded REIT focused solely on investing in farmland. A year later, FPI was formed by Paul Pittman, a partner in a family-owned farming operation in Illinois. Both LAND and FPI lease property to farmers, but LAND is focused more on fresh produce farms in California while FPI is focused on MidWest row crops. Over the past five years, LAND has significantly outperformed FPI, with a return of 12.5% compared to FPI’s -41%. The liquidity benefit of a REIT’s tradability on the stock market also makes it more closely correlated to that market. If stocks go down, REITs are likely to follow suite, whereas farmland typically remains steady or even rises when equities fall.

Mutual Funds and Exchange Traded Funds (ETFs)

Mutual funds and ETFs present another practical option for investors looking to add agriculture to their portfolios. Mutual funds are actively managed or passively chosen portfolios of stocks, bonds, and other securities that invest a portion of a shareholders’ money into related sectors, although it is important to note that no actively managed fund tracked by Morningstar invests exclusively in agriculture. The Invesco DB Agriculture Fund, comprised mostly of commodities, is one of the largest ag-focused mutual funds. The fund is down by nearly 5% over the last 10 years, largely due to depressed commodity prices, trade wars with China, and weather volatility. Many of these mutual funds charge fees and have exposure to other agriculture-related firms and products, so interested investors must decide how much pure farmland exposure they want compared to other ag-related products (crop inputs, technology, equipment, distribution, processing, etc).

Agricultural ETFs can also be actively or passively managed and are comprised of a diversified set of ag businesses who derive substantial portions of their revenues from farming or related agricultural endeavors. The VanEck Vectors Agribusiness ETF is the largest agricultural index fund and returned an annual average of 7.3% for the last 10 years ending in September. Like mutual funds, investors should carefully consider each EFT’s management fees and the performance of the index they track.

Crowdfunding

Unlike the investment options described above, crowdfunding is a relatively new concept when it comes to alternatives ag investing, signed into law as part of the Jumpstart Our Business Startups (JOBS) Act of 2012. As a law intended to encourage funding of small businesses in the US by easing securities regulations, Title III of the act – the CROWDFUND Act – has drawn notable attention. This law created a way for companies to use crowdfunding to issue securities, something not previously permitted.

Historically, when a farmer or agribusiness operator needed to raise capital for expansion or improvements, the only options outside friends and family were traditional ag lenders or in some cases, venture capitalists. The problem is that there are a limited number of ag-specific lenders and the criteria for loan approval has become increasingly more strict with each passing year. In addition to customary lending requirements, demonstration of a farmer’s skills and experience are often necessary, as well as a character evaluation to determine if any “moral hazard risks” exist. This is often coupled with mandatory non-real-estate collateral assignments, personal guarantees, liens on crops, co-signers, and subrogation of existing first-level loans or financing arrangements.

Crowdfunding presents an opportunity for business owners to solicit capital from a much larger pool of smaller investors with fewer restrictions while providing investors the opportunity to add agriculture to their portfolios with less up-front capital and greater liquidity. Specifically, with equity crowdfunding, the investor receives shares of a company in exchange for money pledged. In agriculture, these companies can perform a variety of functions – farmland operation, ownership with outsourced management, agribusinesses across crop types and the value chain, and more.

Unlike traditional equity shares, however, crowdfunding investors are not given voting rights or any other decision-making capabilities with respect to the day-to-day operations of the company. Additionally, the JOBS Act implemented restrictions on how much money non-accredited investors can invest over the course of a given year, based on the individual’s income and net worth. The purpose of these limitations was to prevent less sophisticated and non-accredited investors from taking on too much risk and potentially threatening the stability of their financial future.

What is Available Today and Is It Right for Me?

There are several ag crowdfunding platforms on the marketplace today. Founded in October 2016 and based in Fort Worth, Texas, Harvest Returns is an equity crowdfunding platform dedicated to ag investments. According to their CEO Chris Rawley, Harvest Returns provides “flexible debt and equity funding for specialty farmers while making access to private placements in agribusiness more accessible to investors.” Unlike FarmTogether and FarmFundr, Harvest Returns offers international deals to a userbase of over 3,700 subscribers. To date, Harvest Returns has raised US$2.3 million across three continents and seven projects, including cacao in Ghana and Belize, cattle in Kansas and Georgia, bamboo in Florida, organic hemp CBD in Colorado, and hydroponic produce in Kentucky. One of their current offerings is a Sustainable Agriculture Opportunity Zone Fund focused on the US (starting at $25,000). The company charges listing fees to syndicators to keep the deal live on the platform as well as carried interest from the offerings. Minimum investments into deals range from $5,000 to $25,000. The risks associated with this approach are the capability of the management team to execute on their offering and the liquidity of the investor’s shares of the LLC or SPV. However, many of these platforms are trying to solve this by building large user-bases to whom they can offer rights-of-first-refusal to should another investor need/want to exit. Most of the deals require some lock-up period for funds.

FarmFundr led by Brandon Silveira, is an equity crowdfunding platform focused on specialty crop operations in the US. Founded in February 2016 and based in Fresno, California, FarmFundr chose to differentiate itself by offering farmland ownership opportunities to investors while contracting out the operational management. This approach is common overseas including cacao in Belize and specialty crops in Panama, but FarmFundr is the first to have US offerings. According to Silveira, “we hire a farm manager to handle everyday operations and decisions. Instead of lease income, our investors have ownership of the property, the crop, and the profits.” FarmFundr’s business model charges a fee on capital raised, from the sponsor as well as the investor. According to Silveira, “something that makes us unique is that we pre-fund farmland offerings with no fees to the investor. Instead, we retain an equity position and share the risk alongside our investors.” Both FarmFundr and FarmTogether offer the ability to pre-fund offerings and to date, all three firms take equity positions in the deals they fund. Minimum investments into deals range from $10,000 to $30,000 and current options include an almond orchard, pistachio development and a row crop farm, all in California. This approach does come with the inherent operational risk of owning farmland directly, exposes the investor to commodity price fluctuations, and presents the challenge of liquidating a fractional percent of a larger operation.

Led by Artem Milinchuk, FarmTogether was founded in late 2017 and also focuses on US farmland as an asset class. FarmTogether’s model is one where investment offerings are legal entities, typically LLCs, that own titles to the investment properties. When FarmTogether investors commits capital into a deal, they purchase shares in an LLC and become fractional owners of the farmland property, entitling them to the property’s returns from operations and/or rental income. This is the same model employed by Harvest Returns. Investments on the platform generally start at $25,000, and their platform currently has two crowdfunding opportunities available: a row crop property and a mandarin property. The company also offers separately managed accounts and facilitates 1031 transfers for clients looking to invest $500,000 or more into farmland. Based in San Francisco, California, FarmTogether closed its first offering in September 2019, an almond orchard in Merced County, California, which was 30% oversubscribed. According to Milinchuk, FarmTogether’s two biggest differentiators are their team and technology. “Our team is comprised of investment professionals who have institutional-investment expertise at marquis firms including Prudential, Ontario Teachers’ Pension Plan, and AMERRA Capital.” Milinchuk is also utilizing technology to source deals and perform diligence, the only ag-focused crowdfunding platform to do so. “Our tech team is building an AI-enabled sourcing and diligence engine to assist us in identifying properties for acquisition and capital improvement.” Through AI, Milinchuk expects to decrease due diligence expenses and increase returns for clients. The model generates fees from the services provided to clients and typically includes reimbursements for administrative costs related to the acquisition and management of the property.

The Risks

As with any investment methodology, its merits and risks must be weighed against an investor’s return expectations and risk tolerance. The softening of registration requirements combined with the ease of publication and promotion for deals to non-accredited investors, presents the opportunity within equity crowdfunding for illegitimate actors to solicit investors with lower quality projects. As a result of looser oversight, the possibility for loss of principle with crowd-funded deals is greater than with other alternatives.

The JOBS Act does not leave investors to fend completely for themselves, however, still limiting the amount of money a syndicator can raise in a 12-month period to $1 million, and requires syndicators to either use a qualified intermediary (internet platform registered with the SEC as a broker/dealer) or a newly created Funding Portal, also required to be registered and regulated by the SEC. Investors can change their minds within 48 hours of the close of the raise and syndicators are required to provide annual reports to the SEC.

Investors must carefully weigh the risks and rewards of investing in a new sector like crowdfunding before jumping in. It is advisable that they consult a financial professional or expert in the sector to help guide them through the process.

Conclusion

The inevitabilities of a growing middle class, changing demands for higher quality foods, entrenched consumer concerns with sustainability and traceability, and the continued competition for key resources are all unmistakable value drivers that underpin the agricultural sector, particularly farmland. In order to rise to these challenges, agricultural producers will need to innovate, an endeavor requiring substantial financial outlays from investors who understand the importance of food production. Equity crowdfunding platforms are slowly emerging as solutions where more investors can help contribute to these necessary innovations at lower costs to entry and greater liquidity while reaping the rewards of an expanding sector.

One of the key functions of capital markets is to direct investment dollars into companies and projects solving complex problems. It is difficult to argue with the gravity of the situation facing our farmers today – feeding a population expected to grow by nearly 40 percent in the next 30 years on less land and with concerns over the water supply. It should come as no surprise then that investment dollars have been pouring into the biological and precision agricultural sectors – two key components of the ag value chain with the ability to both increase yield and positively mitigate against harsh weather conditions during the growing season. Even with the exponential growth in these subsectors, agriculture remains one of the least capitalized and mysterious alternative asset classes. Many investors remain skeptical of incorporating it into their portfolios because of a lack of clarity as to how it fits into their investment strategy, limited liquidity, and from a fear of volatility due to direct commodity exposure. The reality is that the long-term trends within the sector are firmly entrenched as key value drivers, offering accessible opportunities to investors willing to explore diversification across the value chain. Biologicals and precision agriculture provide two such opportunities. Michael DeSa of AGD Consulting with Jeremy Stoud, agricultural investment analyst with Bonnefield write for New Ag International.

FINDING THE RIGHT STREAM

Within the agricultural value chain, there are a number of different opportunities for both return generation and capital preservation. The upstream segment of the ag value chain includes inputs to agriculture, such as seeds, crop inputs, machinery, technology and farmland. Three in particular have grabbed investors’ attention recently: biologicals, precision technology and farmland (which is beyond the purview of New Ag International). Biologicals are crop input products derived from naturally occurring chemicals and/or living organisms. Precision ag technology consists of a host of technologies designed to enhance the practice of farming, whether growing crops or raising livestock.

Investing in these sectors is generally regarded as a higher risk and therefore commands higher returns – a potentially attractive proposition to an experienced investor looking to exploit early-mover advantages. According to a March 2018 article published by Forbes on the biological sector in agriculture, biologicals have expanded their sales at a compound annual growth rate (CAGR) of around 17 percent1. Investors are often drawn to this sector by compelling profit margins, which can be as high as 20 to 40 percent2. These kinds of products tend to be lower in toxicity then traditional synthetic chemistries, impact the environment in a generally “softer” manner, and can be developed in a shorter time period with fewer developmental dollars3 . While there are still challenges with the lack of harmonization across regulatory organizations, market fragmentation, top-level consolidation, and a competitive landscape dominated by large multi- nationals, these products will remain an important tool in the farmer’s diversified toolbox employed to boost, or even maintain, yields in a sustainable manner. Precision ag technology has been one of the most innovative and disruptive sectors within the asset class. Advances in computer vision, artificial intelligence and analytical software have fundamentally transformed the operational processes and expectations within the industry. Estimates show that the global precision farming market is expected to reach US$10.23 billion by 2025 with a forecasted CAGR of 14.2 percent4, highlighting a prolonged interest in this sector from a base of around US$1.29 billion in 2015, according to estimates from GrandView Research.

MILLENNIAL INFLUENCE

A significant proportion of the driving force behind the incorporation of new technology into the farm has come from millennials. With 60 percent of U.S. farmers over the age of 555, many are looking for someone new to take up the mantle. According to the Ag America Leading’s 2017 Fast Facts about Agriculture informational page, millennial farmers make up eight percent of U.S. farmers6 with this number growing every year. Couple that with the fact that 20 percent of all current farmers are considered “beginning farmers” (less than 10 years of farming experience) and it becomes easy to see the impact of the millennial mindset on the ag industry. The pressures of resource scarcity, increasing population and changing dietary demands will continue to benefit the ag technology sector as young, innovative producers produce more food with less water, fewer traditional chemicals and with less impact on biodiversity.

SPREADING THE LOAD

Allocation is often an area that new investors find challenging. Some investors see only the growth projections within the broader sector and interpret lower adoption rates as an indication that an opportunity remains to capitalize on the future growth. In certain trends this may be true (aquaculture, alternative meats, impact investing), but in others the ship has already sailed (current variable rate technologies, farm management software and GPS guidance). The precision ag tech market has been so saturated for so long in North America, with many of the products not living up to company claims, that fewer farmers are adopting certain technologies. Couple this with depressed commodity prices, and an environment has been created where many farmers find themselves with just enough free cash to incorporate only the technology absolutely necessary to make it through the next growing season.

The ag biologicals market, as another example, has lower barriers to entry which is one reason that nearly 500 companies have entered this market in the last 10 years7. However, these companies only account for around five percent of the global market for products used in growing crops, and if demand for these product increases there should be room for new entrants. Investors need to fully understand the market dynamics affecting a particular sector within agriculture before allocating capital to a perceived opportunity. A holistic approach to the entire value chain, coupled with a firm understanding of the investor’s risk tolerance and return profiles are required in order to be successful. Asset and portfolio managers must understand the risk profile an investor is willing to assume. As an example, in order to minimize the risks associated with an ag investment into an emerging market (EM), investors need to first parse this risk at a country level, then isolate localized risks that may not be readily apparent at the country-level assessment phase. Some of the greatest risks revolve around politics, macroeconomics and rule of law. While there is little that can be done to manage political and macroeconomic risks, investors need to fully assess these environments, understand all possible scenarios, and make the right tradeoff for themselves between potential risks and rewards.

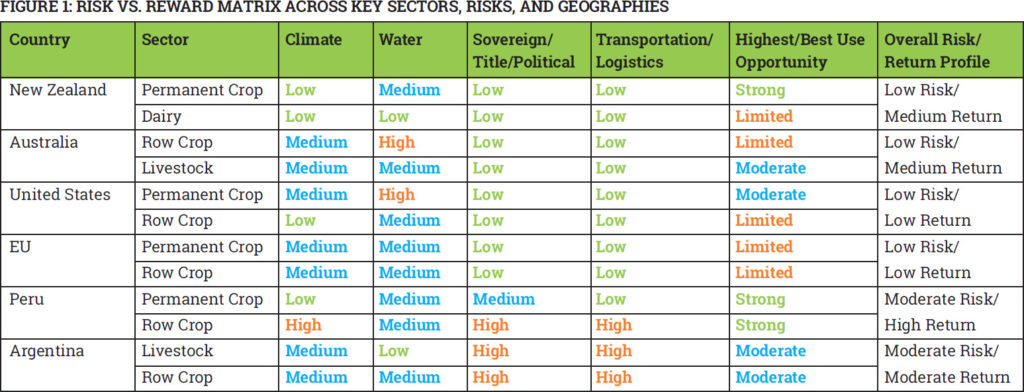

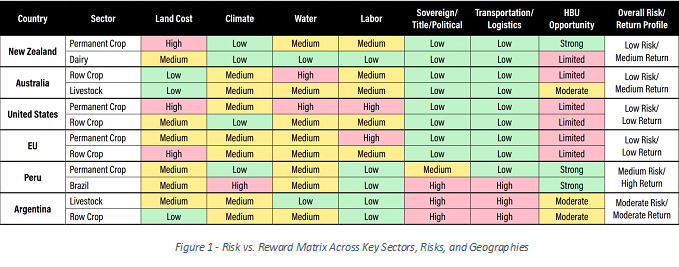

The below matrix highlights key risk parameters and corresponding return profiles for investing in major agriculture regions throughout the world. High water risk in Australia’s row crop and the U.S. permanent crop sectors offer opportunity for precision technology to help mitigate aspects of this risk through more efficient application and monitoring, and more accurate weather predictive modeling. Limited best-use opportunity in the U.S. and European row crop sectors opens a wide window for both precision technology and biologicals to step in and boost yields, support healthier soil profiles, reduce chemicals usage and create more efficiency throughout the production cycle.

Source: Rock IslandLLC and AGD proprietary research, interviews and experience

DOING THE DILIGENCE

A lack of understanding around the different diligence components of each sub-asset class can negatively impact returns and project success over the long-term. Whether the investor performs the diligence themselves or retains a group to do it for them, this remains a critical component of the process. Investors in production farmland do not need operator-level expertise to be successful, but they should know enough about the crop type to know when a tactical, on-farm decision could clash with their overall strategy. They should also consider utilizing a production-based benchmark in order to compare land values across geographies as there tends to be wide variations in farmland productivity and land valuations. A proven de-risking strategy to farmland investing is to partner with an experienced farm operator who has deep country and crop expertise, then spend time conducting diligence on the operator first followed by the asset second. Picking the right partner in an EM is more difficult and often requires boots-on-the-ground experience by the investor or a local team member dedicated to sourcing the best operator from within their trusted network. Finally, it is paramount for investors to understand the relationship between different components of the ag value chain as these present opportunities for de-risking and diversification. Upstream assets are positively correlated to prices, so if the price of corn rises, farm incomes go up and farmers are more likely to spend money on technology, inputs, improvements and expansion. However, as you go downstream, the relationship to price is inverted as processors have significant fixed assets so they tend to do their best when harvests are abundant and prices are low. Strong harvests mean they can run at higher capacity but at a detriment to the farmer who likely sold that commodity to an off-taker at a lower price. It is imperative for investors to understand the interrelationships within the value chain, common misconceptions about the asset class, and how to mitigate identified risks.

HOW TO GET STARTED

Over the past 10 years, individual investors, family offices, private equity, pension funds and even international sovereign wealth funds have begun to realize the value proposition inherent in agriculture. Advances in logistics, storage, processing, technology and management practices have each played a role in opening this asset class to investors of all types.

There are a range of investment structures at varying price points available to both retail and institutional investors. At the retail level, the May 2017 Jumpstart Our Business Startups Act (JOBS Act) established crowdfunding provisions that allow early-stage businesses to offer and sell securities. This Act helped spawn a host of ag-focused crowdfunding and syndication platforms such as Harvest Returns, FarmTogether and FarmFundr, allowing retail investors and family offices to participate in larger ag projects at lower-cost entry points. These platforms vary in the types of investment opportunities offered, geographic focus, and structure and aim to capitalize on the same success of the democratization of the real estate market through groups like Reality Shares in the early 2000s.

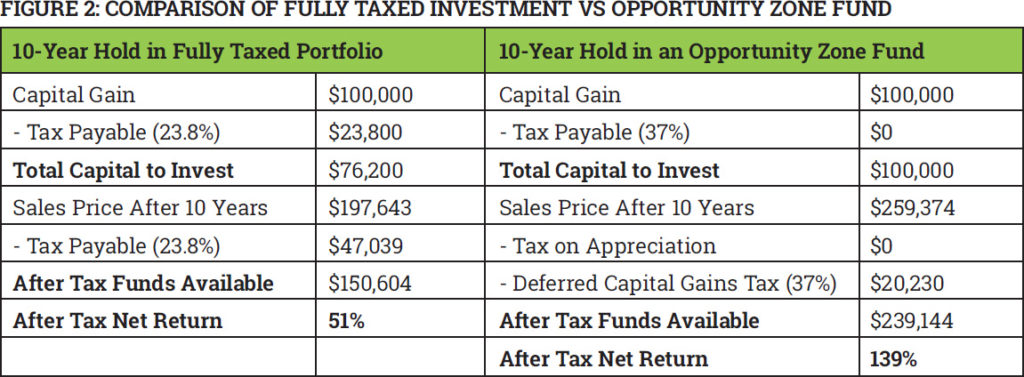

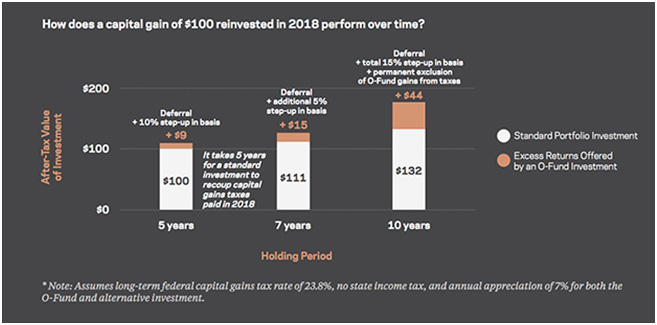

The recent establishment of “opportunity zones” in the United States, targeting economically distressed communities where new investments may be eligible for preferential tax treatments, have also helped foster the creation of ag- specific opportunity zone funds for individual and institutional investors alike. With an investment into an opportunity zone, either directly or through a fund, capital gains from the sale of any asset (if reinvested in 180 days) are deferred until the sale of the new asset, or Dec. 31, 2026, whichever is earlier. Additionally, any re- investment held for five years gets a tax basis increase of 10 percent and any investment held for seven years is 15 percent. Finally, as depicted in Figure 2, investments held for 10 years pay no capital gains tax on the post-acquisition gains. Within the precision ag and biologicals sectors, this could take the practical form of a biologics processing facility, tolling manufacturer or an agtech start-up headquartered in an opportunity zone from which investment dollars will create local jobs and economic incentives within the community. Returns from these types of investments generally materialize within a five- to seven-year timeframe thereby deferring capital gains tax events for investors. If that capital gained is reinvested, there is further opportunity for tax basis increase and capital gains tax decreases.

*Based on 7% annual investment appreciation, no state income tax, and long-term federal combined capital gains tax rate of 23.8%. Source: Seven Peaks Ventures & Harvest Returns.

THE RISE OF PE

Private equity (PE) is largely new to the agribusiness sector, but over the last 15 years there has been a steady rise of PE groups taking positions within the global food and agriculture space throughout the value chain. From 2005 to 2014, more than 200 new investment funds began operating in the food and ag sector, accounting for approximately US$44 billion in assets under management8. According to Prequin’s Special Report on Agriculture from September 2016, several of the world’s largest private equity firms, including Paine & Partners, Proterra, Altima, AMERRA and Blue Road Capital raised a total of US$6 billion across 11 funds9. In October 2014, the chemical manufacturing company, Platform Specialty Products, acquired Ireland-based chemical and biologicals maker Arysta LifeSciences for US$3.51 billion. This deal brought an end to PE firm Permira’s six-year involvement in Arysta, which originally acquired the company back in March 2008 for US$2.4 billion. This sale yielded Permira a 70 percent return on their initial capital in only six years, not including the stake it will retain in Platform10. This summer, a U.S. PE fund managing US$3.7 billion in assets – Metalmark Capital – increased its stake in Valagro S.p.A., a world leader in biostimulant solutions for farmers. The fund first invested in Valagro in October 2016, acquiring a 15 percent stake through a capital increase11.

Since the basis of PE is direct investment into a company, a large initial capital outlay is required, which is why this segment tends to be dominated by larger funds. It is paramount, however, that new-to-ag PE funds tailor their return profiles, timelines and risk tolerances to align with those of the selected sub-sector and geographic region(s). For example, a California-based permanent crop operation is likely not well aligned with a PE firm that wants geographic diversification, 20+ percent net internal rate of return (IRR) and whose exit timeline is five to seven years. However, a PE group looking to achieve 20 to 30 percent net IRRs with a timeline greater than seven years and a developmental focus could be well matched with a soybean crushing expansion project in Brazil or an irrigated blueberry development project in Peru. As typical PE exit multiples, timelines and return profiles are not generally well aligned with direct ownership of commodity crop models, these funds tend to focus on biologicals and precision ag, land conversion and development, infrastructure, logistics, value-added processing and storage assets.

CONCLUSIONS

Whatever the investment thesis, geographic preference, return profile, risk tolerance or investor type, the ag value chain has the spectrum of opportunity to offer something for everyone. The uncorrelated nature of the asset class when compared to equities or bonds, its tangibility, preservation of wealth characteristics and return profiles offer a natural inflation hedge and diversification to the traditional paper markets. The inevitabilities of a growing middle class in China and India, and the global population at large, including changing demands for higher quality foods, entrenched consumer concerns with sustainability and traceability, and the continued competition for key resources are all unmistakable value drivers that underpin the agricultural sector as a resilient and viable asset class.

Food is one of mankind’s most basic survival needs and yet, the means by which is it produced, is largely misunderstood and underrepresented by the investment community. Agriculture is one of the oldest investment sectors in the world, time-tested and proven to weather economic uncertainty. Yet even today as farmland is widely acknowledged as an alternative investment, many investors are skeptical of incorporating it into their portfolios because of a lack of clarity as to how it fits into their investment strategy, concerns over liquidity,and from a fear of volatility due to direct commodity exposure. The reality is that the long-term trends within this sector are firmly entrenched as key value drivers, offering accessible opportunities to investors willing to explore diversification across the value chain.

With the global population expected to reach nearly 10 billion by 2050, the development of a robust food system will not only be crucial to ensuring this larger population is nourished, but force the lands and systems which produce these necessities to remain economically viable. Demand for food is outpacing population growth as global eating habits continue to evolve from a predominantly vegetable diet to a mix of animal-based proteins and more nutritious fruits and vegetables. Global meat consumption per capita more than doubled from 20 kg per year in 1961 to 42 kg in 2014[1] while the annual global population growth rate slowed by nearly 20 percent[2]. As we move through a greater frequency and variety of dietary changes, additional land will be required to produce the necessary food profiles. Competition for key resources such as water and arable land will continue to drive innovation and efficiencies while changing consumer values and ethical stances on food production are likely to further bolster long-term demand for more sustainable agriculture. All of these factors are net positive for a strong investment sentiment within the global food and agriculture sector for years to come.

Investment Opportunities Abound Across the Asset Class

Within the agricultural value chain, there are a number of different opportunities for both return generation and capital preservation, each with unique investment characteristics.The upstream segment of the ag value chain includes inputs to agriculture, such as seeds, crop inputs, machinery, technology, and farmland. Three in particular have grabbed investors’ attention recently: biologicals, precision technology, and farmland. Biologicals are crop input products derived from naturally occurring chemicals and/or living organisms. Precision ag technology consists of a host of technologies designed to make the practice of farming more accurate and controlled when it comes to growing crops and raising livestock. These two sectors are generally regarded as a higher risk and therefore command higher returns – a potentially attractive proposition to an experienced investor looking to exploit early-mover advantages. According to a March 2018 article published by Forbes on the biological sector in agriculture, biologicals have expanded their sales at a compound annual growth rate (CAGR) of around 17 percent[3]. Investors are often drawn to this sector by compelling profit margins, which can be as high as 20 to 40 percent[4].

Source: MarketsandMarkets

These kinds of products

tend to be lower in toxicity then traditional synthetic chemistries, impact the

environment in a generally “softer” manner, and can be developed in a shorter

time period with fewer developmental dollars[5].

While there are still challenges with the lack of harmonization across

regulatory organizations, market fragmentation, top-level consolidation, and a

competitive landscape dominated by large multi-nationals, these products will

remain an important tool in the farmer’s diversified toolbox employed to

enhance yields in a sustainable manner.

Precision ag technology

has been one of the most innovative and disruptive sectorswithin the asset

class. Advances in computer vision, artificial intelligence, and analytical

software have fundamentally transformed the operational processes and

expectations within the industry. Estimates show that the global precision

farming market is expected to reach US$10.23B by2025 with a forecasted CAGR of

14.2 percent[6],

highlighting a continued interest in this sector.

A significant proportion of

the driving force behind the incorporation of new technology into the farm has

come from millennials. With sixty percent of US farmers over the age of 55[7],many

are looking for someone new to take up the mantle. According to the Ag America

Leading’s 2017 Fast Facts about Agriculture informational page, millennial

farmers make up eight percent of US farmers[8]

with this number growing every year. Couple that with the fact that 20 percent

of all current farmers are considered “beginning farmers” (less than ten years

of farming experience) and it becomes easy to see the impact of the millennial

mindset on the ag industry. The pressures of resource scarcity, increasing

population,and changing dietary demands will continue to benefit the ag

technology sector as young, innovative producers produce more food with less

water, fewer traditional chemicals, and with less impact on biodiversity.

Production agriculture includes animal protein, aquaculture, and of course,farmland. Farmland in particular has historically proven itself as a tangible, long-term, stable store of wealth, appreciating nearly nine percent annually over the last seventy years in North America[9]. A Global Farmland Index developed by Savills World Research and illustrated by the dotted line in the graph below is comprised of data from 15 key farmland markets across the globe. This index highlights an average annualized growth since 2002 of 13.3 percent.The strong, steady growth also illustrates a reduced volatility when compared with other key commodities.

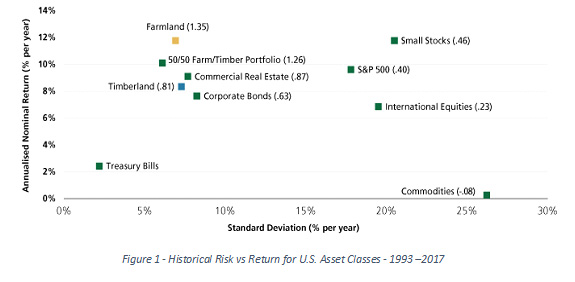

When compared to other selected asset classes within the US markets and global commodities, farmland and timberland have upheld their reputation as uncorrelated, low risk asset classes with strong annualized real returns. Additionally, as a “real asset”, farmland will never reach a nominal value of zero so long as it remains productive.

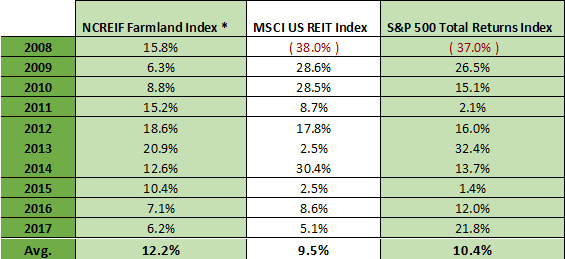

When compared to the

S&P 500, the market index that represents approximately 80 percent of the

value of the US stock market, farmland investments outperformed the S&P

over a 10-year span. As the graph below

illustrates, the 2008 financial crisis had virtually no impact on the NCREIF

Farmland Index’ investment value, further highlighting agriculture as a secure,

stable alternative uncorrelated with the equities market.

Market

Index Comparison – Annual Returns 2008 – 2017

Note: * Consists of 727 U.S. agricultural properties woth approximately US$8.5 billon Sources: National Council of Real Estate Investment Fiduciaries (NCREIF), TIAA/University of Illinois – Center for Farmland Research (Correlation and standard deviation data from 1970-2016)

Finally, mid and downstream opportunities within the sector offer additional ways for investors to capitalize on several eminent macroeconomic drivers. Large harvest yields generally lead to lower commodity prices due to market saturation, but for downstream groups such as traders, processors, packagers, retail distributors, and wholesalers, this means their processing plants may operate at a greater capacity, while input materials are reduced in cost. Full plants and slaughter houses can lead to additional revenue and stronger returns for investors. Mid and down stream investments provide investors with less naked commodity risk and if diversified across crop type and geography, can serve as a hedge against the cyclical nature of the agriculture asset class.

Investing across the value

chain can be synergistic and reduce intermediation and inefficiency costs. Attractive

agribusiness opportunities are available across the globe, if you know where to

look and what to avoid.

Myths, Misconceptions and Means of Mitigation

Agriculture can be

misunderstood as an asset class. Illiquidity can be seen as an obstacle and value

chain components may be taken in isolation, painting an incomplete picture of the

risks and rewards. Capital is often misallocated and misaligned given a

particular risk tolerance and the diligence required around the different

components of an asset is frequently not fully understood or performed.

Illiquidity is often cited as a primary reason for avoiding the sector all together. There are, however, creative options for liquidity in this sector. Secondary markets for farmland are becoming a real possibility for private investors as the customer base for ag-focused crowdfunding platforms and parceled ownership structures increase. The larger these decentralized investment platforms become and the more parcel owners there are within a given plantation, the more buyers there are should an investor need/want to exit. Lower interest rates have also opened the door on the debt side for increased allocations to ag lenders. According to the Federal Reserve Bank of Kansas City, total non-real estate farm loans were up nearly eight percent from a year ago. This was the seventh consecutive quarter of annual growth in loan volumes with an average growth rate in 2018 of about 12 percent[10]. Real Estate Investment Trusts (REIT) offer additional opportunities for retail investors to participate in the ag sector with higher liquidity options. Gladstone Land Corporation (LAND) for example, is one of two publically-traded Farm REITs. Finally, many institutional investors are also looking closely at higher-value permanent crops with longer production life cycles. These business models typically involve the development of greenfield plantations with 10-15 year off-take agreements. This long-term approach offers a strong return over a given time period while simultaneously providing lower price volatility for the off-taker, although they can carry higher operational risk.

Allocation is often an area new investors find challenging.Within the agtech sector for example, some see only the growth projections within the broader sector and interpret lower adoption rates as an indication that an opportunity remains to capitalize on the future growth. In certain trends this may be true (aquaculture, alternative meats, impact investing), but in others the ship has already sailed (current variable rate technologies, farm management software and GPS guidance).The precision agtech market has been so saturated for so long in North America, with many of the products not living up to company claims, that fewer farmers are adopting certain technologies. Couple this with depressed commodity prices, and you’ve created an environment where many farmers find themselves with just enough free cash to incorporate only the technology absolutely necessary to make it through the next growing season. The ag biologicals market, as another example, has lower barriers to entry which is one reason that nearly 500 companies have entered this market in the last ten years. However, these companies only account for around five percent of the global market for products used in growing crops[11], leaving ample room for continued expansion. Investors need to fully understand the market dynamics affecting a particular sector within agriculture before allocating capital to a perceived opportunity. A holistic approach to the entire value chain, coupled with a firm understanding of the investor’s risk tolerance and return profiles are required in order to be successful.

When considering developed vs emerging market investments, one of the key differences is the risk profile an investor is willing to assume. An investment in Latin American farmland or agribusiness project, for example, may present a higher risk profile, but these risks are becoming increasingly easier to understand and mitigate. To minimize these risks, investors need to first parse emerging market risk at a country-level, then isolate specific, often localized risks that may not be readily apparent at the country-level assessment phase. Some of the greatest risks revolve around politics, macroeconomics, and rule of law. While there is little that can be done to manage political and macroeconomic risks, investors need to fully assess these environments, understand all possible scenarios, and make the right trade-off for themselves between potential risks and rewards. The below matrix highlights key risk parameters and corresponding return profiles for farmland investing in major agriculture regions throughout the world.

A lack of understanding around the different diligence components of each sub-asset class can negatively impact returns and project success over the long-term.Whether the investor performs the diligence themselves or retains a group to do it for them, this remains a critical component of the process. An investor in production farmland does not need operator-level expertise to be successful, but they should know enough about the crop type to know when a tactical, on-farm decision could clash with their overall strategy. They should also consider utilizing a production-based benchmark in order to compare land values across geographies as there tends to be wide variations in farmland productivity and land valuations. A proven de-risking strategy to farmland investing is to partner with an experienced farm operator who has deep country and crop expertise, then spend time conducting diligence on the operator first then the asset second. This can work for a US investment group looking to invest in soybeans in Brazil or cattle in Australia. Picking the right partner in an emerging market is more difficult and often requires boots-on-the-ground experience by the investor or a local team member dedicated to sourcing the best operator from within their trusted network.

Finally, it is paramount for investors to understand the relationship between different components of the ag value chain as these present opportunities for de-risking and diversification. Upstream assets are positively correlated to prices, so if the price of corn rises for example, farm incomes go up and farmers are more likely to spend money on technology,inputs, improvements, and/or expansion. However, as you go downstream, the relationship to price is inverted with processors having significant fixed assets, so they tend to do their best when harvests are abundant, which often leads to lower prices. Strong harvests mean they can run at higher capacity, but at a detriment to the farmer, who likely sold that commodity to an off-taker at a lower price. It is imperative for investors to understand the interrelationships within the value chain, common misconceptions about the asset class, and how to mitigate identified risks.

How to Get Started

Over the past ten years, individual investors, family offices, private equity, state pension and retirement funds, and even international sovereign wealth funds have begun to realize the value proposition inherent in agriculture. Advances in logistics, storage, processing, technology and management practices have each played a role in opening up this asset class to investors of all types.

There are a range of options, scale, structures and price points available to both retail and institutional investors.At the retail level, the May 2017 Jumpstart Our Business Startups Act (JOBS Act) established crowdfunding provisions that allow early-stage businesses to offer and sell securities. This Act helped spawn a host of ag-focused crowdfunding and syndication platforms such as Harvest Returns, FarmTogether, FarmFundr, and Farmland Partners allowing retail investors and family offices to participate in larger ag projects at lower-cost entry points. These platforms vary in the types of investment opportunities offered, geographic focus, and structure and aim to capitalize on the same success of the democratization of the real estate market through groups like Reality Shares in the early 2000s. The recent establishment of “opportunity zones” in the United States as well, targeting economically distressed communities where new investments may be eligible for preferential tax treatments, have also helped foster the creation of ag-specific opportunity zone funds for individual and institutional investors alike.

Figure 4 – Incentives Offered by the Opportunity Zone Program

Often, the simplest and most direct way to gain exposure to farmland is to either own/operate the land yourself, own the land and outsource the management, or purchase the land directly, then lease it back to an operator. According to the 2016 Preqin Special Report on Agriculture, 90 percent of investors in agriculture/farmland are open to land-owner focused opportunities. If a first-time farmland investor prefers to own/operate the land directly, it is advisable to do so on-site and in partnership with a management company for the first few years until the owner becomes comfortable with all aspects of running the operation. Direct ownership comes with increased exposure to the cyclicality of commodity prices, disease/pest issues and water management challenges, but if done correctly, more of the top-line falls directly to the owner. If an investor wants the tangibility of direct farmland exposure, but limited operational risk, there are structures available both domestically and internationally where investors can own titled parcels of farmland that aggregate to form large plantations with economies of scale. These structures can achieve operational efficiencies and cost savings without the logistical burden falling directly to the owner. Most come with embedded management contracts, so the investor does not have to be an experienced operator in order to benefit from direct farmland ownership. Sale/lease back models can also be attractive to private and certain institutional investors, so long as there are clear rights of tenure and land use agreements between the landowner and leasee. These can be more challenging if the landowner is an absentee owner and while lease agreements typically do not incentive the leasee to care for or develop the farmland long-term, it can be an attractive way for an investor to earn near-passive income from a farmland investment.

Private Equity (PE) is largely new to the agribusiness sector, but over the last ten to fifteen years there has been a steady rise of PE groups taking positions within the global food and agriculture space throughout the value chain. From 2005 to 2014, more than 200 new investment funds began operating in the food and ag sector, accounting for approximately US$44 billion in assets under management[12]. According to Prequin’s Special Report on Agriculture from September 2016, several of the world’s largest private equity firms, including Paine & Partners, Proterra, Altima, AMERRA and Blue Road Capital raised a total of $6B across 11 funds in the last ten years for ag/farmland funds[13]. Since the basis of PEis direct investment into a company or farmland operation, a large initial capital outlay is required, which is why this segment tends to be dominated by larger funds. It is paramount however that a new-to-ag PE funds tailor their return profiles, timelines and risk tolerances to align with those of the selected sub-sector and geographic region(s). For example, a California-based permanent crop operation is likely not well aligned with a PE firm who wants geographic diversification, 20+ percent net IRRs and whose exit timeline is five to seven years. That being said, a PE group looking to achieve 20-30 percent net IRRs with an exit in five to seven years and a developmental focus could be well matched with a soybean crushing expansion project in Brazil or an irrigated blueberry development project in Peru.As typical PE exit multiples, timelines and return profiles are not generally aligned with direct ownership of commodity crop models, these funds tend to focus on biologicals and precision ag, land conversion and development, infrastructure, logistics, value-added processing, and storage assets. There is nothing fundamentally wrong with favoring a niche or business model within the broader ag sector, as long as there is diversification elsewhere in the fund.

Investing in productive farmland at an institutional scale, particularly for pension funds with longer time horizons, has been historically difficult due to asset fragmentation, low turnover, geographic diversity and a high degree of differentiation between various commodity types. Often times, more patient capital prefers to acquire large, contiguous, farms with steady cashflows. As these farms are typically offered through a competitive bidding process, this naturally drives up acquisition prices,compressing return projections for an investor who prefers more reliable cashflows. Therefore, some funds are seeking groups that have access to a continuous stream of proprietary, off-market, and mid-sized deals which offer low acquisition prices, more room for development and opportunity to diversify.

Conclusions

Whatever the investment

thesis, geographic preference, return profile, risk tolerance or investor type,

the ag value chain has the spectrum of opportunity to offer something for

everyone. The uncorrelated nature of the asset class, its tangibility, preservation

of wealth possibilities, and return profiles in emerging markets offer a natural

inflation hedge and diversification to the traditional paper markets. The

inevitabilities of a growing middle class and the population at large,

including changing demands for higher quality foods, entrenched consumer

concerns with sustainability and traceability, and the continued competition

for key resources are all unmistakable value drivers that underpin the

agricultural sector as a resilient and viable asset class.

Primary Author – Michael DeSa is the Founder/Managing Director of AGD Consulting, a veteran-owned strategic agribusiness advisory firm servicing the global food/agriculture investment and technology sectors. His agricultural engineering background, 10-years of project management experience with the U.S. Marine Corps, and agribusiness investment experience make him uniquely qualified to counsel companies throughout the region.

Contributing

Author – Jeremy Stoud is an agricultural

investment analyst with Bonnefield based in Toronto, Canada. With a background

in international food business, he offers insights on global agri-food and

water investments, value chain analysis and economic systems. He has

volunteered and worked with a spectrum of primary and vertically integrated

agricultural groups in North and South America, Europe and Africa.

[2] The World Bank. “Population growth (annual %). Population source: (

1 ) United Nations Population Division. World Population Prospects: 2017

Revision, ( 2 ) Census reports and other statistical publications from national

statistical offices, ( 3 ) Eurostat: Demographic Statistics, ( 4 ) United

Nations Statistical Division. Population and Vital Statistics Report ( various

years ), ( 5 ) U.S. Census Bureau: International Database, and ( 6 )

Secretariat of the Pacific Community: Statistics and Demography Program.https://data.worldbank.org/indicator/SP.POP.GROW?end=2014&start=1960&view=chart

This is the third article in an eight-part series published by GAI News that examines eight existing trends set to alter the structure of our global food system. Join us each month for a new installment, and be sure to read the first two articles here: Part I, Part II.

“In all affairs it’s a healthy thing now and then to hang a question mark on the things you have long taken for granted.” – Bertrand Russell

There is every reason for us as consumers to pause and consider something that is far too often taken for granted – water. It has become a truism to say that civilization would not exist without the reliability of our earth’s accessible water resources. Our species’ ability to evolve past a Paleolithic state is a direct result of our advances in freshwater use, from leveraging gravity for flood irrigation, to controlling water flow with aqueducts, to the implementation of digitally-integrated irrigation systems.

Societal reliance on fresh water has been presupposed for so many centuries that many of us overlook the ongoing constraints set to fundamentally alter the way we use this scarce resource. This article aims to review a few of the many water challenges affecting the global agri-food sector and places a spotlight on investable regions which may weather the storm most effectively.

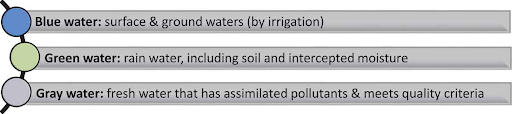

When assessing freshwater availability, it is essential to consider the components of the water system within and beyond human control. The thought of addressing all water challenges may be an overwhelmingly broad topic, so the conversation becomes more actionable when we focus on components that can be changed rather than those that cannot. Of freshwater stores, ‘blue water’ is the most pertinent topic to international agriculture as we have little control over deviation in rainwater occurrence and quantity. Water scientists place particular emphasis on blue water within the context of a changing climate – namely as it pertains to projected increases in the frequency and severity of global drought.(1)

Common Freshwater Classification(2)

Less than 3 percent of the earth’s total water stock is fresh water and nearly four-fifths of the 3 percent are permanently frozen and inaccessible.(3) After factoring in areas of excessive pollution, acidity, and salinization we are left with less than one-tenth of a percent of fresh water supply available for human, agriculture, and industry use.(4) In other words, this equates to about 10,000,000 cubic km of fresh, accessible ground and surface water.(5) While freshwater is limited in volume, humans are continuing to increase consumption per capita on an annual basis(6), and at a pace that far exceeds the rate of replenishment.(7) Here lies the bone of contention. It is not a question of whether we are using scarce water resources at an unsustainable pace, but rather a discussion of what can be done about it.

Blue Water – Consumable and Irrigatable

Water use for irrigation is among the most heavily contested aspects of the modern agricultural system. Agriculture and blue water depletion are inextricably linked. According to a recent report from Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES), nearly 75 percent of the world’s accessible freshwater consumption is dedicated to crop and livestock production and nearly 40 percent of the planet’s current food supply is reliant on irrigation.(8) This issue becomes further pronounced when we consider that nearly half of the world’s population is living within immediate proximity to river basins and aquifers with the ‘severe water stress’ classification.(9) Evidence suggests that over usage and maltreatment of accessible freshwater resources could cause a contraction in global productivity growth, and therefore a potential decline in living standards.(10)

Most of our planet’s accessible fresh water is confined in shallow aquifers beneath the earth’s surface. A high proportion of these non-renewable aquifers are reaching critical points of depletion, and they are commonly located in areas which fall beneath the world’s most populous and important agricultural regions. A study from the Proceedings of the National Academy of Science estimates that up to 100 million irrigated acres may be unable to draw sufficient water resources to support production by the end of the century.(11) This could lead to drastic decreases in crop yields if rainfall averages cannot make up the difference. The Ogallala aquifer beneath the U.S. Corn Belt, for example, is particularly threatened by overuse and pollutant contamination. A reversal of irrigated land to dryland is expected to occur in regions such as California’s central valleys, the U.S. Midwest, the North-China Plain, and the Arabian Basin. In each of these regions, non-renewable groundwater is a primary source of irrigation. It is not coincidental that each of these regions have been subject to significant water stress in the past decade.

Blue water depletion is a complex issue that demands collective action – not solvable by implementing any single policy, action, or framework, but rather it requires a cooperation between all levels of business, government, and society. Irrigated farms that source their water from continually measured, renewable deposits (such as sustainably disbursed lakes and river systems) may be the most productive, economical, and sustainable solution to the forthcoming water scarcity challenges.

Virtual Water

Consumers may look at food-induced water depletion as a direct product of farm activity, while the reality is more complex and integrates all facets of society. Farmers, like any other business, are economic entities that aim to optimize output, scale, and profitability. In the agri-food sector this is accomplished by efficiently fulfilling the needs of consumers. With a growing population and an increasing appetite for high-quality proteins, fruits, and vegetables, consumers tend not to realize the macro-effects of their individual purchasing decisions, but rather focus on the needs of the household or community.

As it stands, we have a developed consumer base that is unaware that we effectively outsource water depletion through our demand for high water-footprint foods.(12) An often cited example is China’s import of water-intensive soybeans from areas such as Brazil, which has led to indirect pressure on deforestation of the Amazon.(13) We have historically been able to purchase food and industrial products with the cost of water extraction embedded in the price, but often not the true cost of water depletion. This distinction is vital to the topic of global water management, where governments often subsidize industry water use as a regular cost of doing business in order to provide consumers with food options that meet their demands.

Most experts believe these consumer trends towards high-footprint foods are firmly established, although as shoppers begin to realize the increased demands on water is a result of their decisions, they too may begin to search for more sustainable and renewable ways to use the available water supply. It is here where we see a long-term investable opportunity.

Farmland Investing: Go Where the Renewable Water Flows

The pursuit of a sustainable and profitable agricultural investment portfolio may be achieved through consideration of macro-climatic indicators, strategic selection, and rigorous due diligence. While this article refers to agricultural investing from a farmland perspective, there also is a case to be made for investments in agricultural technology, including efficient irrigation, wastewater reuse, soil moisture sensing, and seed resilience technologies.

A structural decline in crop production is expected to create supply shocks in the future, potentially raising agricultural commodity prices in the long term. The Intergovernmental Panel on Climate Change (IPCC) estimates that crop yields could decline by up to 12 percent as a consequence of water scarcity in the next three decades.(14) The thesis of investing in ‘water-rich’ regions is predicated upon their capacity to weather an incoming storm of potential water issues:

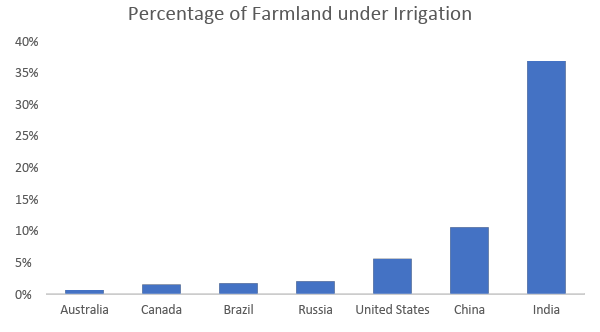

~ Invest where irrigation is less necessary for productive agriculture: Less than 4 percent of Canada, Brazil, Russia, and Australia’s farmland is irrigated compared to about 10 percent in the United States and 37 percent in India (15)(See Figure 2). Productive agricultural regions that are less dependent on irrigation tend to hedge the risk of groundwater depletion and/or pollution.

Figure 2: Percentage of Farmland Under Irrigation(16)

Source: The World Bank World Development Indicators, 2015

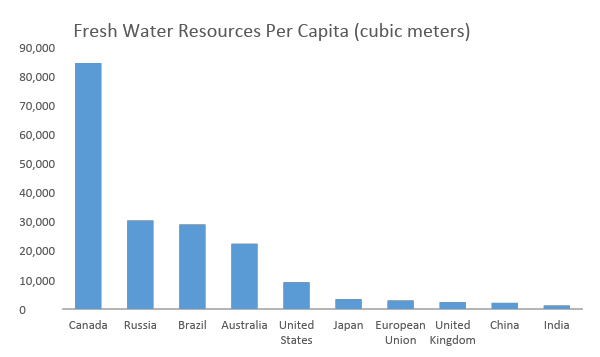

~ Analyze metrics to determine where water shortages are expected to fall: Statistics such as renewable fresh water per capita are helpful in determining where water crises are expected to occur. Other helpful statistics include aquifer replenishment rates, variable on-farm water requirements, and the legal parameters of water resource allocation. While Canada, Russia, Australia, and Brazil use relatively little water for irrigation compared to the rest of the world, they hold the most fresh water reserves per capita of all agricultural exporters with 80,200 cubic meters.(17) Further projections suggest that warm-climate regions are likely to experience decreasing precipitation levels in the next century while polar and continental regions may encounter more rainfall.(18) Although each country’s water rights laws and natural precipitation levels may vary, the thesis holds over a long-term geographic perspective while political frameworks may change. This sentiment should be further examined at a regional level to assess where irrigating farmland may be achieved most sustainably.

Figure 4: Global Freshwater Resources per Capita(19)

Source: The World Bank, 2014

For as long as humans inhabit the planet, unpolluted, fresh, water will be a finite resource with limited supply and consistent demand. Although specific water reserves appear to have promise over the next several decades, it is a responsibility for farm owners, governments, consumers, and investors to responsibly regulate withdrawal and avert contamination. Freshwater depletion is an agricultural issue just as much as it is an environmental one. Here lies a rare circumstance where economic returns may be matched by environmental impact. Agricultural investors have a distinct opportunity to allocate capital towards efficient irrigation and farmland portfolios in regions that have the replenishing capacity to withdraw water resources sustainably.

ABOUT THE AUTHORS

PRIMARY AUTHORJeremy Stroud is an agricultural investment analyst with Bonnefield based in Toronto, Canada. With a background in international food business, he offers insights on global agri-food and water investments, value chain analysis and economic systems. He has volunteered and worked with a spectrum of primary and vertically integrated agricultural groups in North and South America, Europe and Africa.

CONTRIBUTING AUTHOR

Michael DeSa is the founder/managing director of AGD Consulting, a U.S.-based, strategic advisory and business development firm servicing the agricultural and resource sectors in emerging and OECD markets. His agricultural engineering background, 10-years of project management experience with the U.S. Marine Corps, and agribusiness investment experience make him uniquely qualified to counsel companies throughout the region.

This is the second article in an eight-part series to be published by GAI News that will examine the eight existing trends that are set to alter the structure of our global food system. Join us each month for a new installment, and see the first article here.

“The nation that destroys its soil destroys itself.” – F.D. Roosevelt

The oft-imagined idea of fertile, pristine farmland as far as the eye can see is drifting towards the past. Land loss is more than just a blow to those who grasp on to a pastoral ideal of the countryside; rather it marks a shift in the global supply dynamics of land resources. The literature presents a singular case: more topsoil is removed from production than is added, with some academics estimating a reduction of about 1 percent each year[1].

Healthy topsoil is home to billions of thriving micro-organisms which allow crops to be optimally produced. As the top soil is physically eroded or disrupted, its biological matter also declines, and therefore its capacity to produce optimal yields is compromised.

Land scarcity is not a new concept, although with the level of impact it is expected to have on society, it is a topic that deserves more discussion. In the first article of this series, we discussed the effects of urbanization on the global agricultural system. This commentary will examine another piece of the farmland usage puzzle and its impact on our collective accessibility to food: land degradation and soil erosion.

Land degradation refers to human-derived processes which lead to the decline in ecosystem functions[2]. It manifests itself in three different forms:

physical: compaction, desertification, and soil erosion (which is the largest contributor to productivity loss)

chemical: soil acidification and salinization

biological: soil organic matter reduction and loss in biodiversity

Farmers work in different ways to combat chemical and biological forms of land degradation, although the most persistent and arguably the most difficult to mitigate of these, is physical degradation of topsoil. While usually considered as a local concern, soil erosion, compaction and other types of land degradation are globally consequential issues and evidence suggests they will have direct implications for the world’s food supply.

The Inter-Governmental Science-Policy Platform on Biodiversity and Ecosystem Services (IPBES) is widely considered the international authority on bio-ecological matters[3]. The organization recently concluded a three-year study analyzing the status of global land and soil quality, which collected insights from over one hundred of the world’s leading subject experts. They found that approximately 3.2 billion people, or nearly 43 percent of the world’s population, experience negative economic impacts from land degradation in industries varying from agriculture to tourism, to mining[4]. The effects of land degradation are expected to accelerate in magnitude as the degree of high-volatility weather systems increase[5].

The Causes and Status of Land Degradation Globally

Erosion takes place when soil is left uncovered and the particles are washed or blown away. Heavy downpours, surface water ponding, intensive land use and mechanical human activities are continuing to reduce top soil – particularly in the most intensively farmed regions. For example, China and India are losing topsoil at three to four times the rate of North America[6]. Land erosion and degradation also occurs due to tillage, deforestation, and an increase in rainfall intensity. One study indicates that there has been a 53 percent increase in the number of extreme rainfall days recorded globally over the past 30 years, thereby leading to record levels of erosion and runoff[7].

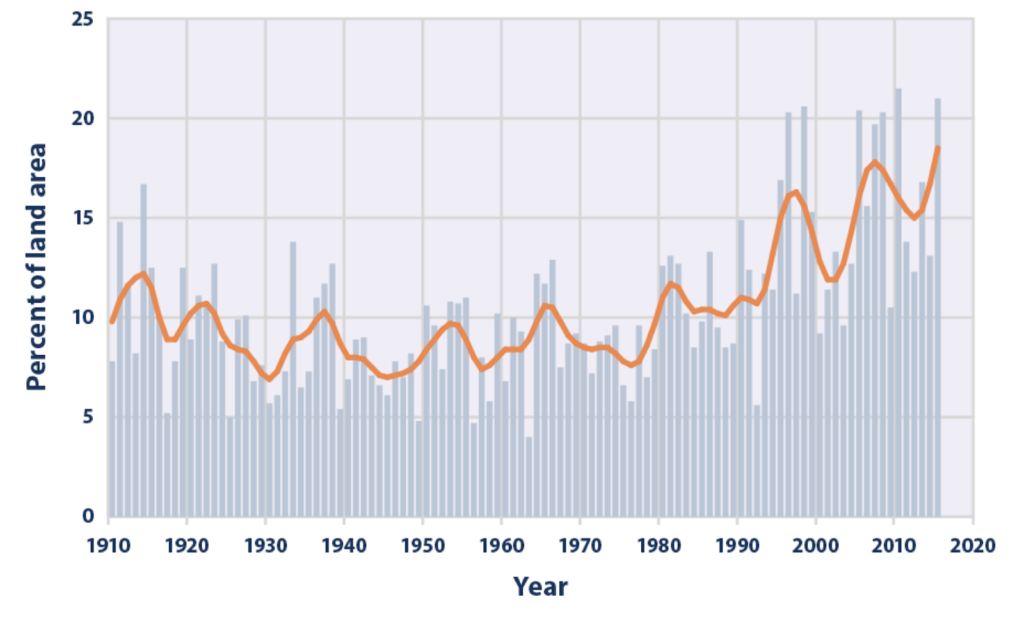

In the past 20 years, a greater proportion of rainfall has arrived in the form of extreme single-day weather events than has ever been recorded. Figure 1 demonstrates the percentage of land area in the contiguous United States affected by extreme precipitation in each year as reported by the National Oceanic and Atmospheric Administration. The orange line represents a nine-year trailing average, highlighting a significant fact for soil erosion: the average percentage of US land affected by extreme one-day rain events has increased from 7 percent in the 1970’s to 18 percent in 2015.

Figure 1: Extreme One-Day Weather Events in the Contiguous United States, 1910-2015[8]

Erosion naturally leads to further soil compaction, nutrient degradation and impaired water drainage, which reduces the overall productive capacity of the land. With nearly 60 percent of the world’s farmland considered degraded, our arable land base is steadily declining[9].

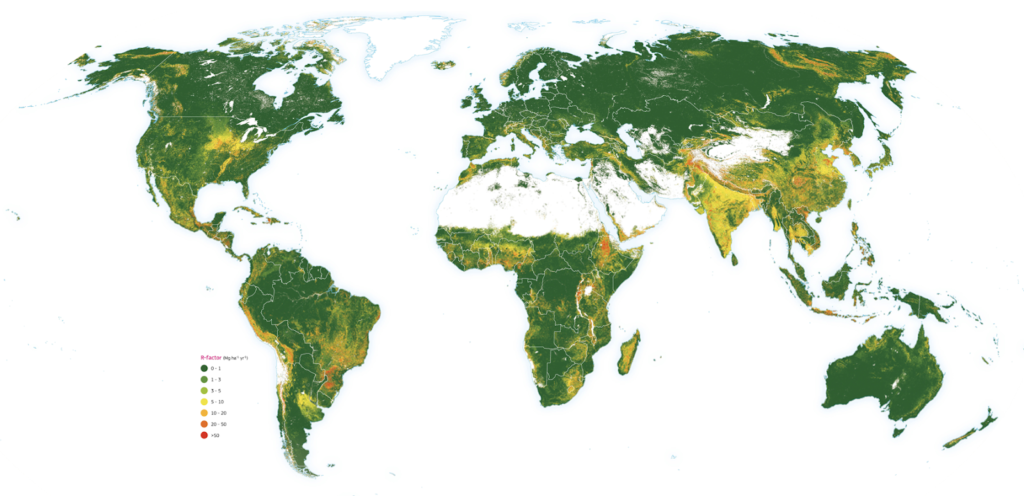

Figure 2 demonstrates where the greatest soil erosion concerns are expected to occur in the future based on a detailed joint study by the European Commission and the University of Basel. The R-factor is the rainfall-runoff erosivity factor, or an annual summation of erosion index (EI) values (erosion force of rainfall) in a normal year’s rain.

Figure 2: The Geo-Spatial Pattern of Soil Erosion, 2018[10]

Opportunity Amidst the Loss

As soil degradation increases the scarcity of fertile land, it also creates the need to incorporate sustainable farm management practices and pursue responsible investment goals. Farmland investors and stakeholders should consider five primary categories in their path to mitigate soil erosion effects and potentially reap the upside potential that follows:

1.) Deal Sourcing & Region Identification: Investors should look to identify farming regions with topsoil abundance, low wind and flood risk, and relatively flat or rolling terrain. Investment teams have the responsibility to review an area’s historical and forecasted climatic risks in advance of deal selection. This includes past precipitation and temperature averages, available soil and yield mapping data, historical input usage, previous environmental issues and/or remediation measures. Investors may also want to consider geographic regions that successfully practice no-till land preparation, such as Argentina, Australia, and Canada.

2.) Due Diligence: Most farmland asset managers should be able to leverage geo-spatial information data and measurement tools to determine how past farm imagery compares to the current status of the field. It is also worthwhile to consider warning signs such as noticeable compaction, dispersed ponding, and natural drainage flows.

3.) Sustainable Farm Management Practices: Farm operators have the opportunity to replenish topsoil quality through the implementation of practices such as no-till and low-till farming, as well as the regular use of green manure crops to enhance soil biodiversity, structure, and to replenish nutrients. Further, integrated pest management (IPM) plans leveraging biological and mechanical processes can control pests while reducing chemical pesticide use.

4.) Investment in Loss Prevention & Restoration: Capital expenditure in ditching, tile drainage, external tree-borders, berms, and riparian-buffer maintenance can control soil erosion effects while also mitigating natural disaster risks such as flooding, wind damage, and surface ponding. For permanent and specialty crop strategies, the implementation of technology and products offered by groups like the Land Life Company – a startup that is working to restore ecosystems in degraded soil regions through reforestation efforts – should be considered CapEx well spent.[14]

5.) Long-term Tenure Mindset: Investors who plan to own and/or operate farmland for the long-term will be naturally incentivized to adopt sustainable land management practices which can promote the health and productivity of soil. Farmland owners should be cautious of short-term (less than three year) lease structures which may create the risks of nutrient mining or high-intensity agricultural practices.

With land degradation on the rise, the tools to reduce soil loss and protect these investments are slowly becoming more available and adoptable. As soils from intensive agricultural regions continue to deplete, we hypothesize that land managed with sustainable practices shall prove to be significantly more valuable in the decades to come.

ABOUT THE AUTHORS:

PRIMARY AUTHOR

Jeremy Stroud is an agricultural investment analyst with Bonnefield based in Toronto, Canada. With a background in international food business, he offers insights on global agri-food and water investments, value chain analysis and economic systems. His travels have brought him to over 50 countries – within which he has volunteered and worked with a spectrum of primary and vertically integrated agricultural businesses.

CONTRIBUTING AUTHOR

Michael DeSa is the founder/managing director of AGD Consulting, a U.S.-based, strategic advisory and business development firm servicing the agricultural and resource sectors in emerging and OECD markets. His agricultural engineering background, 10-years of project management experience with the U.S. Marine Corps, and agribusiness investment experience make him uniquely qualified to counsel companies throughout the region.

This is the first article in an eight-part series to be published by GAI News that will examine the eight existing trends that are set to alter the structure of our global food system. Join us each month for a new installment.

It is no secret that our global food system is in a state of flux. In the next century, we will be challenged to produce more food with less land, by fewer farmers, and with increasingly scarce water resources. Although evidence suggests that we as humans have the capacity to achieve this, it is imperative to explore what changes can be expected from the planet’s climatic and demographic variability. The purpose of this article series is to provide insight on these changes and place a spotlight on the regions which may weather the change most effectively. While other parts of the world are projected to experience comparatively strenuous conditions, parts of the Canadian and U.S. agricultural systems are positioned to endure and even prosper in the face of a changing climate and demographic.

A combination of industry and academic literature indicates eight existing trends that are set to alter the structure of our global food system. A growing body of data indicates that these factors may determine our collective success or failure:

1. Urban expansion

2. Land erosion and degradation

3. Fresh water scarcity and agriculture’s reliance on irrigation

4. Increasing temperatures and CO2 levels

5. Volatility of weather systems

6. Global phosphate over-use

7. Bee fatalities and pollination

8. Population growth in proportion to arable land