One of the key functions of capital markets is to direct investment dollars into companies and projects solving complex problems. It is difficult to argue with the gravity of the situation facing our farmers today – feeding a population expected to grow by nearly 40 percent in the next 30 years on less land and with concerns over the water supply. It should come as no surprise then that investment dollars have been pouring into the biological and precision agricultural sectors – two key components of the ag value chain with the ability to both increase yield and positively mitigate against harsh weather conditions during the growing season. Even with the exponential growth in these subsectors, agriculture remains one of the least capitalized and mysterious alternative asset classes. Many investors remain skeptical of incorporating it into their portfolios because of a lack of clarity as to how it fits into their investment strategy, limited liquidity, and from a fear of volatility due to direct commodity exposure. The reality is that the long-term trends within the sector are firmly entrenched as key value drivers, offering accessible opportunities to investors willing to explore diversification across the value chain. Biologicals and precision agriculture provide two such opportunities. Michael DeSa of AGD Consulting with Jeremy Stoud, agricultural investment analyst with Bonnefield write for New Ag International.

FINDING THE RIGHT STREAM

Within the agricultural value chain, there are a number of different opportunities for both return generation and capital preservation. The upstream segment of the ag value chain includes inputs to agriculture, such as seeds, crop inputs, machinery, technology and farmland. Three in particular have grabbed investors’ attention recently: biologicals, precision technology and farmland (which is beyond the purview of New Ag International). Biologicals are crop input products derived from naturally occurring chemicals and/or living organisms. Precision ag technology consists of a host of technologies designed to enhance the practice of farming, whether growing crops or raising livestock.

Investing in these sectors is generally regarded as a higher risk and therefore commands higher returns – a potentially attractive proposition to an experienced investor looking to exploit early-mover advantages. According to a March 2018 article published by Forbes on the biological sector in agriculture, biologicals have expanded their sales at a compound annual growth rate (CAGR) of around 17 percent1. Investors are often drawn to this sector by compelling profit margins, which can be as high as 20 to 40 percent2. These kinds of products tend to be lower in toxicity then traditional synthetic chemistries, impact the environment in a generally “softer” manner, and can be developed in a shorter time period with fewer developmental dollars3 . While there are still challenges with the lack of harmonization across regulatory organizations, market fragmentation, top-level consolidation, and a competitive landscape dominated by large multi- nationals, these products will remain an important tool in the farmer’s diversified toolbox employed to boost, or even maintain, yields in a sustainable manner. Precision ag technology has been one of the most innovative and disruptive sectors within the asset class. Advances in computer vision, artificial intelligence and analytical software have fundamentally transformed the operational processes and expectations within the industry. Estimates show that the global precision farming market is expected to reach US$10.23 billion by 2025 with a forecasted CAGR of 14.2 percent4, highlighting a prolonged interest in this sector from a base of around US$1.29 billion in 2015, according to estimates from GrandView Research.

MILLENNIAL INFLUENCE

A significant proportion of the driving force behind the incorporation of new technology into the farm has come from millennials. With 60 percent of U.S. farmers over the age of 555, many are looking for someone new to take up the mantle. According to the Ag America Leading’s 2017 Fast Facts about Agriculture informational page, millennial farmers make up eight percent of U.S. farmers6 with this number growing every year. Couple that with the fact that 20 percent of all current farmers are considered “beginning farmers” (less than 10 years of farming experience) and it becomes easy to see the impact of the millennial mindset on the ag industry. The pressures of resource scarcity, increasing population and changing dietary demands will continue to benefit the ag technology sector as young, innovative producers produce more food with less water, fewer traditional chemicals and with less impact on biodiversity.

SPREADING THE LOAD

Allocation is often an area that new investors find challenging. Some investors see only the growth projections within the broader sector and interpret lower adoption rates as an indication that an opportunity remains to capitalize on the future growth. In certain trends this may be true (aquaculture, alternative meats, impact investing), but in others the ship has already sailed (current variable rate technologies, farm management software and GPS guidance). The precision ag tech market has been so saturated for so long in North America, with many of the products not living up to company claims, that fewer farmers are adopting certain technologies. Couple this with depressed commodity prices, and an environment has been created where many farmers find themselves with just enough free cash to incorporate only the technology absolutely necessary to make it through the next growing season.

The ag biologicals market, as another example, has lower barriers to entry which is one reason that nearly 500 companies have entered this market in the last 10 years7. However, these companies only account for around five percent of the global market for products used in growing crops, and if demand for these product increases there should be room for new entrants. Investors need to fully understand the market dynamics affecting a particular sector within agriculture before allocating capital to a perceived opportunity. A holistic approach to the entire value chain, coupled with a firm understanding of the investor’s risk tolerance and return profiles are required in order to be successful. Asset and portfolio managers must understand the risk profile an investor is willing to assume. As an example, in order to minimize the risks associated with an ag investment into an emerging market (EM), investors need to first parse this risk at a country level, then isolate localized risks that may not be readily apparent at the country-level assessment phase. Some of the greatest risks revolve around politics, macroeconomics and rule of law. While there is little that can be done to manage political and macroeconomic risks, investors need to fully assess these environments, understand all possible scenarios, and make the right tradeoff for themselves between potential risks and rewards.

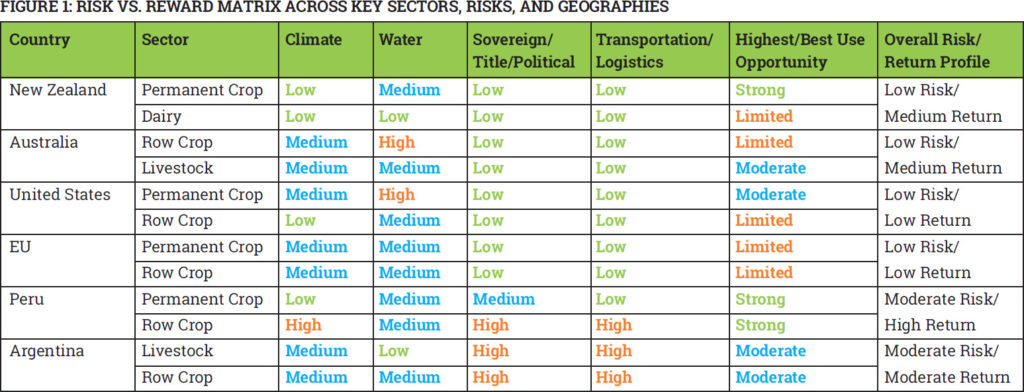

The below matrix highlights key risk parameters and corresponding return profiles for investing in major agriculture regions throughout the world. High water risk in Australia’s row crop and the U.S. permanent crop sectors offer opportunity for precision technology to help mitigate aspects of this risk through more efficient application and monitoring, and more accurate weather predictive modeling. Limited best-use opportunity in the U.S. and European row crop sectors opens a wide window for both precision technology and biologicals to step in and boost yields, support healthier soil profiles, reduce chemicals usage and create more efficiency throughout the production cycle.

DOING THE DILIGENCE

A lack of understanding around the different diligence components of each sub-asset class can negatively impact returns and project success over the long-term. Whether the investor performs the diligence themselves or retains a group to do it for them, this remains a critical component of the process. Investors in production farmland do not need operator-level expertise to be successful, but they should know enough about the crop type to know when a tactical, on-farm decision could clash with their overall strategy. They should also consider utilizing a production-based benchmark in order to compare land values across geographies as there tends to be wide variations in farmland productivity and land valuations. A proven de-risking strategy to farmland investing is to partner with an experienced farm operator who has deep country and crop expertise, then spend time conducting diligence on the operator first followed by the asset second. Picking the right partner in an EM is more difficult and often requires boots-on-the-ground experience by the investor or a local team member dedicated to sourcing the best operator from within their trusted network. Finally, it is paramount for investors to understand the relationship between different components of the ag value chain as these present opportunities for de-risking and diversification. Upstream assets are positively correlated to prices, so if the price of corn rises, farm incomes go up and farmers are more likely to spend money on technology, inputs, improvements and expansion. However, as you go downstream, the relationship to price is inverted as processors have significant fixed assets so they tend to do their best when harvests are abundant and prices are low. Strong harvests mean they can run at higher capacity but at a detriment to the farmer who likely sold that commodity to an off-taker at a lower price. It is imperative for investors to understand the interrelationships within the value chain, common misconceptions about the asset class, and how to mitigate identified risks.

HOW TO GET STARTED

Over the past 10 years, individual investors, family offices, private equity, pension funds and even international sovereign wealth funds have begun to realize the value proposition inherent in agriculture. Advances in logistics, storage, processing, technology and management practices have each played a role in opening this asset class to investors of all types.

There are a range of investment structures at varying price points available to both retail and institutional investors. At the retail level, the May 2017 Jumpstart Our Business Startups Act (JOBS Act) established crowdfunding provisions that allow early-stage businesses to offer and sell securities. This Act helped spawn a host of ag-focused crowdfunding and syndication platforms such as Harvest Returns, FarmTogether and FarmFundr, allowing retail investors and family offices to participate in larger ag projects at lower-cost entry points. These platforms vary in the types of investment opportunities offered, geographic focus, and structure and aim to capitalize on the same success of the democratization of the real estate market through groups like Reality Shares in the early 2000s.

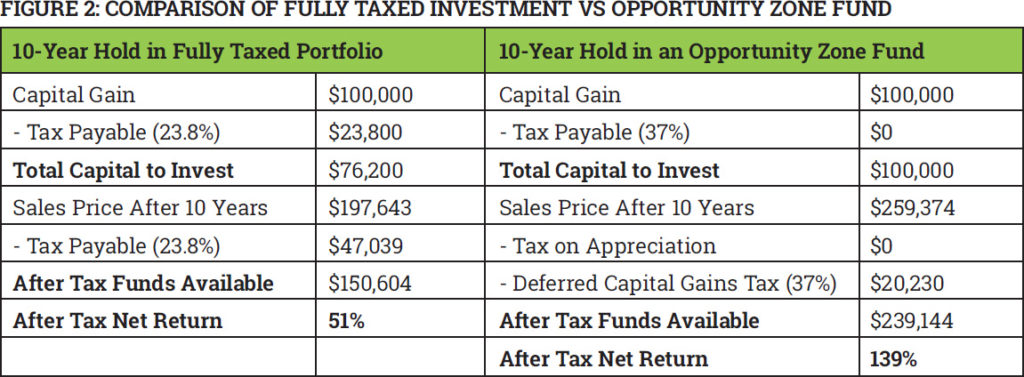

The recent establishment of “opportunity zones” in the United States, targeting economically distressed communities where new investments may be eligible for preferential tax treatments, have also helped foster the creation of ag- specific opportunity zone funds for individual and institutional investors alike. With an investment into an opportunity zone, either directly or through a fund, capital gains from the sale of any asset (if reinvested in 180 days) are deferred until the sale of the new asset, or Dec. 31, 2026, whichever is earlier. Additionally, any re- investment held for five years gets a tax basis increase of 10 percent and any investment held for seven years is 15 percent. Finally, as depicted in Figure 2, investments held for 10 years pay no capital gains tax on the post-acquisition gains. Within the precision ag and biologicals sectors, this could take the practical form of a biologics processing facility, tolling manufacturer or an agtech start-up headquartered in an opportunity zone from which investment dollars will create local jobs and economic incentives within the community. Returns from these types of investments generally materialize within a five- to seven-year timeframe thereby deferring capital gains tax events for investors. If that capital gained is reinvested, there is further opportunity for tax basis increase and capital gains tax decreases.

THE RISE OF PE

Private equity (PE) is largely new to the agribusiness sector, but over the last 15 years there has been a steady rise of PE groups taking positions within the global food and agriculture space throughout the value chain. From 2005 to 2014, more than 200 new investment funds began operating in the food and ag sector, accounting for approximately US$44 billion in assets under management8. According to Prequin’s Special Report on Agriculture from September 2016, several of the world’s largest private equity firms, including Paine & Partners, Proterra, Altima, AMERRA and Blue Road Capital raised a total of US$6 billion across 11 funds9. In October 2014, the chemical manufacturing company, Platform Specialty Products, acquired Ireland-based chemical and biologicals maker Arysta LifeSciences for US$3.51 billion. This deal brought an end to PE firm Permira’s six-year involvement in Arysta, which originally acquired the company back in March 2008 for US$2.4 billion. This sale yielded Permira a 70 percent return on their initial capital in only six years, not including the stake it will retain in Platform10. This summer, a U.S. PE fund managing US$3.7 billion in assets – Metalmark Capital – increased its stake in Valagro S.p.A., a world leader in biostimulant solutions for farmers. The fund first invested in Valagro in October 2016, acquiring a 15 percent stake through a capital increase11.

Since the basis of PE is direct investment into a company, a large initial capital outlay is required, which is why this segment tends to be dominated by larger funds. It is paramount, however, that new-to-ag PE funds tailor their return profiles, timelines and risk tolerances to align with those of the selected sub-sector and geographic region(s). For example, a California-based permanent crop operation is likely not well aligned with a PE firm that wants geographic diversification, 20+ percent net internal rate of return (IRR) and whose exit timeline is five to seven years. However, a PE group looking to achieve 20 to 30 percent net IRRs with a timeline greater than seven years and a developmental focus could be well matched with a soybean crushing expansion project in Brazil or an irrigated blueberry development project in Peru. As typical PE exit multiples, timelines and return profiles are not generally well aligned with direct ownership of commodity crop models, these funds tend to focus on biologicals and precision ag, land conversion and development, infrastructure, logistics, value-added processing and storage assets.

CONCLUSIONS

Whatever the investment thesis, geographic preference, return profile, risk tolerance or investor type, the ag value chain has the spectrum of opportunity to offer something for everyone. The uncorrelated nature of the asset class when compared to equities or bonds, its tangibility, preservation of wealth characteristics and return profiles offer a natural inflation hedge and diversification to the traditional paper markets. The inevitabilities of a growing middle class in China and India, and the global population at large, including changing demands for higher quality foods, entrenched consumer concerns with sustainability and traceability, and the continued competition for key resources are all unmistakable value drivers that underpin the agricultural sector as a resilient and viable asset class.

REFERENCES

1 Savage, Steven. “Updates on the Rapidly Growing Biologicals Sector in Agriculture.” Forbes. 18 March 2018.

https://www.forbes.com/sites/stevensavage/2018/03/15/update-on-therapidly-growing-biologicals-sector-in-agriculture/#50b1865c55be

2 Transparency Market Research. “Global Biologics Market Will be Worth US$479, 752 Million by 2024; Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2016 – 2024. 06 October 2016.

https://www.prnewswire.com/news-releases/global-biologics-market-willbe-worth-us479-752-million-by-2024-global-industry-analysis-size-sharegrowth-trends-and-forecast-2016—2024-tmr-596150181.html

3 Savage, Steven. “Updates on the Rapidly Growing Biologicals Sector in Agriculture.” Forbes. 18 March 2018.

https://www.forbes.com/sites/stevensavage/2018/03/15/update-on-therapidly-growing-biologicals-sector-in-agriculture/#50b1865c55be

4 Grand View Research. “Precision Farming Market Worth $10.23 Billion by 2025 | CAGR 14.2%.” May 2019. https://www.grandviewresearch.com/pressrelease/global-precision-farming-market

5 United States Department of Agriculture. “Beginning Farmers and Age Distribution of Farmers.” 26 April 2019.

https://www.ers.usda.gov/topics/farm-economy/beginningdisadvantaged-farmers/beginning-farmers-and-age-distribution-offarmers/

6 Cubbage, Steve. “Will The Generation That Wants to Change Agriculture Show Up To Work?” Ag Web – Powered by Farm Journal. 11 February 2019.

https://www.agweb.com/article/will-the-generation-that-wants-tochange-agriculture-show-up-to-work/

7 Savage, Steven. “Updates on the Rapidly Growing Biologicals Sector inAgriculture.” Forbes. 18 March 2018.

https://www.forbes.com/sites/stevensavage/2018/03/15/update-on-therapidly-growing-biologicals-sector-in-agriculture/#50b1865c55be

8 Valoral Advisors. “The Rise of Food and Agriculture Private Equity Space.”

September 2014 Report. https://www.valoral.com/wpcontent/uploads/The-Rise-of-the-Food-Agriculture-Private-Equity-Space-September-2014.pdf

9 Preqin. “Preqin Special Report: Agriculture.” September 2016. Accessed 30 May 2019. https://docs.preqin.com/reports/Preqin-Special-Report-Agriculture-September-2016.pdf

10 Summerfield, Richard. Financier Worldwide Magazine. “Permira exits Arysta LifeSciences”. December 2014 Report.

https://www.financierworldwide.com/permira-exits-arystalifescience#.XYIb5ChKiUk

11 Magri, Valentina. “US private equity firm Metalmark raises its stake in Italy’s biostimulant leader Valagro.” Be Beez. Posted June 25, 2019.

https://bebeez.it/en/2019/06/25/us-private-equity-firm-metalmark-raisesits-stake-italys-biostimulants-leader-valagro/