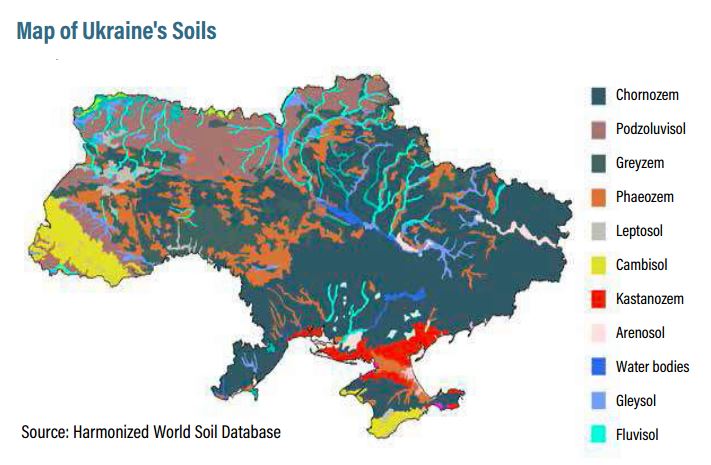

Ukraine’s agricultural production capability is often overshadowed by the country’s civil conflict and lack of business transparency. However, a closer look at this strategically-positioned agricultural powerhouse reveals there is ample opportunity for growth to meet the world’s increasing food requirements. Ukraine is the number two global leader in overall grain exports after the United States and takes the number three seat in corn exports.1 They are the number one producer of sunflower seeds and exporter of sunflower oil, reaching 1.16 billion tons of sunflower seeds produced in 2016/2017.2 Over 70 percent of the country’s total area is agricultural farmland, totaling more than 30 million hectares suitable for agricultural production.3 This level of production is accomplished on less than 10 percent of the total

agricultural farmland in the United States, due in large

part to the quality of soil. Ukraine boasts one of the

richest concentrations of fertile soil on the planet, with

over 30 percent of the world’s reserves of chornozem or

“black earth” lying within its borders. The soil contains

approximately seven to 15 percent organic matter

necessary for quality crop production compared to two to

eight percent in other parts of the world.4

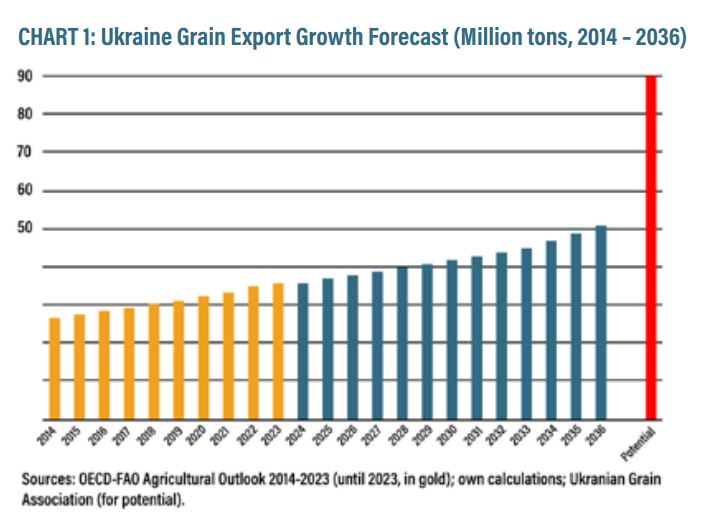

Even with quality soils and ample arable

land, Ukraine is not producing anywhere near

its potential. According to Ukraine’s Deputy

Minister of Agrarian Policy and Food of Ukraine

for European Integration, Olga Trofimtseva, the

country harvested 66 million metric tons of

grain in 2016 and 62 million in 2017.5 She believes

this is far from the limit, commenting that Ukraine

could easily harvest 100 million metric tons in

the coming years, subject to the development

and use of new technology and land reforms.

She isn’t the only one who believes Ukraine is

operating at a production deficit. The Organization

for Economic Cooperation and Development

Food and Agriculture Organization’s Agricultural

Outlook for Ukraine projects Ukraine’s grain

export potential could reach 90 million metric

tons. Note that when the below graph was

produced in 2014, Ukraine had already exceeded

grain export projections for 2017 by nearly 20

million metric tons (see CHART 1).

If Ukraine could reach these production

levels, this would give them an exportable

surplus of approximately 50-60 million metric

tons, assuming 40-50 million for domestic

consumptions.6 An exportable surplus is an

indication of country’s ability to supply a lower

cost product to the global market, thereby

increasing their competitive advantage.

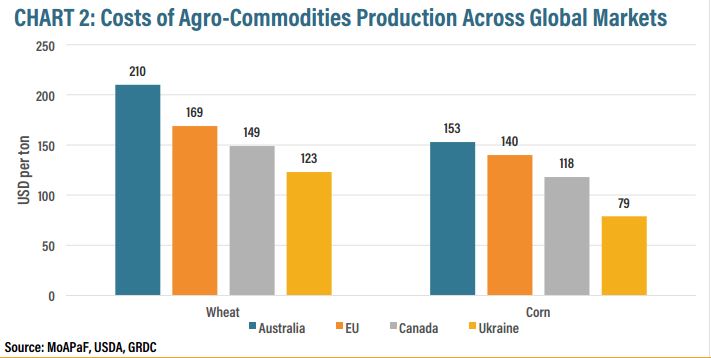

The ability of growers to keep production costs

low can have a significant impact on profitability

and growth potential. A direct comparison of

farmland prices in the Ukraine to other markets

on a cost per hectare basis is inconclusive due

to wide variations in farmland productivity

and land prices, therefore, land cost per unit of

production is a more meaningful comparison

metric. The utilization of a production-based

benchmark allows investors to compare land

values using different production characteristics.

The graph below shows costs of production

for wheat and corn in the Ukraine compared to

several other markets (see CHART 2).

Investing in farmland with low land costs per

unit of production can allow an investor to realize

greater capital gains through the application

of things like new technology and modernized

equipment, experienced management teams, and

to the extent possible in the Ukraine, economies

of scale. It is important to note, however, that this

metric does not take into account the logistical

costs/considerations of getting the commodity

from the farm gate to the marketplace.

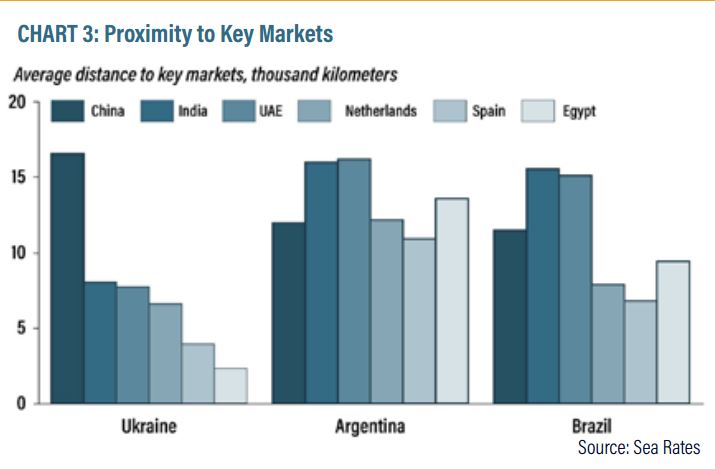

Ukraine’s geographic positioning to key

European and Asian markets also provides

additional cost-saving advantages. The graph

below shows Ukraine’s advantageous positioning

to key export markets (see CHART 3).

Proximity to these markets helps keep

transportation costs low and also provides

steady demand for commodities as middle

classes in places like the EU and China

continue to grow. Finally, a large labor pool – 25

percent of the Ukrainian population is employed

in the agricultural sector7 – providing another

supporting parameter for low-cost

crop production.

High quality, naturally occurring soil – low-cost

per unit of production as a result of strategic

positioning to key markets and a large labor

pool – are all positive indicators of Ukraine’s

agricultural investment potential. The caveat is

that, because of the severe limitations to land

ownership by foreign investors in the Ukraine,

investors should examine opportunities outside

direct farmland investments that still capitalize on

the land’s productivity potential.

OPPORTUNITIES

As grain production forecasts predict a sizable

increase in output from Ukraine, investments will

need to be made into the country’s transportation

and storage infrastructure to support this

increased supply. Logistic costs for moving grain

from Ukrainian farms to the Black Sea ports are

still approximately 40 percent higher than cost

for comparable services in France and Germany,

and 30 percent higher than costs in the United

States.8 These high costs are often the result

of poor logistics, specifically outdated railway

transportation equipment, underutilization of

river transport, and insufficient storage capacity

leading to higher spoilage. As a result, farmers

receive lower shares of the market prices and

shoulder these logistical costs from their own

balance sheets. These losses in annual revenue

potential can range between US$600 million to

US$1.6 billion.9

CATCHING THE TRAIN

A review of the Ukraine railway system reveals

that currently 60 percent of grain volume in the

Ukraine is transported via rail. The country boasts

the 13th largest railway network in the world

and can easily absorb the increased production

forecasts with proper infrastructure development

and equipment improvements (see CHART 4)

For example, current rolling stock of

Ukrzaliznytsia (UZ), the state-owned Ukrainian

monopoly that controls the vast majority of

railroad transportation in the country, is outdated

and ill-equipped. A recent World Bank study

estimated that a US$64 million investment in

Ukraine’s railway infrastructure, including 8,500

grain hoppers, new wagons, and locomotives,

could yield an Estimated Rate of Return (ERR) of

21 percent.10

While transportation from storage to port is

primarily done by rail in the Ukraine, significant

investment is also needed to improve river

and barge infrastructure and deep water port

facilities. Only five percent of exported grain is

moved along Ukrainian rivers, representing a

formidably untapped opportunity to transport

bulk ag products reliably, efficiently, and at a

low cost, especially along the Dnipro River.

River transportation in the Ukraine is often

less expensive and more environmentally

efficient than railway transport, with unitary

transportation costs of three to 8.9 USD per ton

compared to 10.5 for rail and 16.4 for road.11 The

same World Bank study estimated a US$580

million investment could yield a 21 percent ERR.

This would include dredging the Dnipro River’s

shallow bottom to accommodate larger ships and

prevent freezing during peak production winter

months, lock passages, bridges, and port storage

infrastructure. This type of investment could also

lead to a capacity increase of five to six million

tons of grain annually by 2022 and a 30 percent

reduction in costs associated with road damages

by 2022.

Improvement to rail and river transportation

infrastructure will allow Ukrainian producers

to offer even lower cost per unit of production

to offtakers, but grain storage is yet another

key component of the value chain suitable

for foreign investment. Sufficient and quality

grain storage infrastructure will help Ukrainian

farmers minimize loss and store grain longer. In

2014, Ukraine had a grain harvest of nearly 64

million metric tons, however, existing certified

storage infrastructure allowed for immediate

storage of only 45 to 65 percent.12 Many existing

facilities are more than 50 years old while the

complementary infrastructure supporting drying,

loading/unloading, and testing operations are

energy-intensive and employ little to no recent

improvement from precision technology.13

According to the World Bank, a US$1.5 billion

investment into 6.4 million metric tons of new

elevator capacity could reduce grain loss by

15 percent per annum yield and return early

investors a 24 percent ERR. Without appropriate investment, poor logistics will become a bottleneck to sector development rather than a

vehicle of trade facilitation.

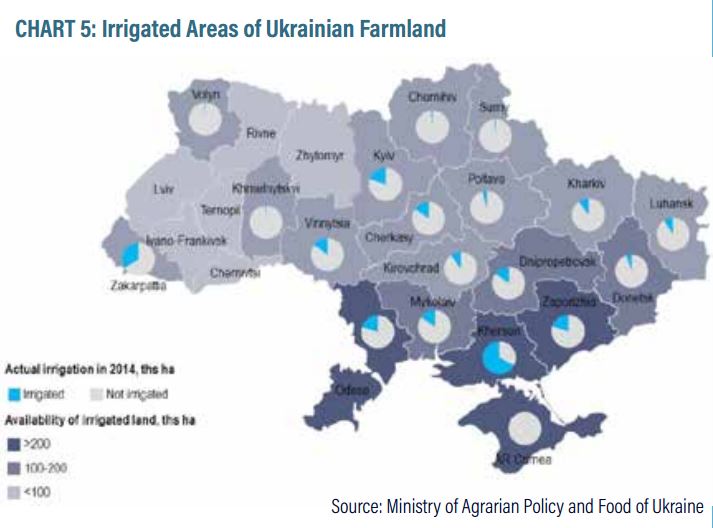

A Fluid Investment

Opportunities exist in the upstream portion of

the Ukrainian ag value chain as well, particularly

in irrigation infrastructure. During the Soviet

era, irrigation was widely used throughout the

country. At one point, irrigation infrastructure

grew by 100,000 hectares per year.14 While

much of this machinery is now dated, proper

maintenance and repurposing on the back of

investment dollars could revitalize millions of

hectares of existing infrastructure. At present,

most Ukrainian farmers use dryland farming

practices which place significant risk at the

mercy of Mother Nature (see CHART 5).

Irrigated land has the potential to produce two

to two-and-a-half times the yield compared to

traditional dryland farming, without the risk of

uncertain precipitation conditions. A recent State

of Nebraska irrigation study showed a yield of

4.7 million tons per acre of corn on irrigated land

compared to a yield of 1.8 million tons per acre

on dryland, resulting in a revenue growth of over

$240 more per irrigated acre. Under the right

structure and management team, this could be

a profitable way to participate in the forecasted

Ukrainian agricultural uplift.

Adding Value with Agtech

Finally, the application of precision technology

to Ukraine’s agricultural sector will further allow

producers to increase yield, reduce production

costs, and optimize input consumption without

the necessity for scale. There should be no doubt

now that agtech is a booming sector across

the globe. According to an August 2018 market

intelligence report released by BIS Research, the

global precision agriculture market is expected

to raise US$10.55 billion by 2025, increasing at a

CAGR of 13.7 percent from 2018 to 2025.15 With only

three to four percent of arable land in the Ukraine

under precision management, there is much

room for growth.16 Early movers to this space

who identify ways to apply precision technology

to Ukrainian farm operations, while limiting their

exposure to country risk, stand to do well.

One such area is soil erosion. According to the

World Bank, Ukraine loses about 50,000 hectares

of farmland every year from soil erosion and land

degradation.17 Groups like AgriEye, a Ukrainian

company founded in 2016, hope to cut this loss

in half through the application of drone imagery,

multispectral remote sensing, and open source

geospatial imaging data. AgriEye uses this

input data to create a precise field map of soil

composition, which it then pairs with algorithms

to analyze yield and provide prescriptive

recommendations on how to irrigate and fertilize.

While they charge for this service internationally,

it’s free to Ukrainian farmers. Other Ukrainian

firms like SmartFarming are applying data-driven

solutions to help Ukrainian farmers reduce

costs by as much as US$3,000 per hectare and

save their producers more than 10 percent of

inventories in a season through the re-equipment

of machinery.18 Associations and accelerators like

AgTech Ukraine, while only a few years old, are

beginning to draw attention to the importance of

technology in the sector.

Adding Value with Agtech

Finally, the application of precision technology

to Ukraine’s agricultural sector will further allow

producers to increase yield, reduce production

costs, and optimize input consumption without

the necessity for scale. There should be no doubt

now that agtech is a booming sector across

the globe. According to an August 2018 market

intelligence report released by BIS Research, the

global precision agriculture market is expected

to raise US$10.55 billion by 2025, increasing at a

CAGR of 13.7 percent from 2018 to 2025.15 With only

three to four percent of arable land in the Ukraine

under precision management, there is much

room for growth.16 Early movers to this space

who identify ways to apply precision technology

to Ukrainian farm operations, while limiting their

exposure to country risk, stand to do well.

One such area is soil erosion. According to the

World Bank, Ukraine loses about 50,000 hectares

of farmland every year from soil erosion and land

degradation.17 Groups like AgriEye, a Ukrainian

company founded in 2016, hope to cut this loss

in half through the application of drone imagery,

multispectral remote sensing, and open source

geospatial imaging data. AgriEye uses this

input data to create a precise field map of soil

composition, which it then pairs with algorithms

to analyze yield and provide prescriptive

recommendations on how to irrigate and fertilize.

While they charge for this service internationally,

it’s free to Ukrainian farmers. Other Ukrainian

firms like SmartFarming are applying data-driven

solutions to help Ukrainian farmers reduce

costs by as much as US$3,000 per hectare and

save their producers more than 10 percent of

inventories in a season through the re-equipment

of machinery.18 Associations and accelerators like

AgTech Ukraine, while only a few years old, are

beginning to draw attention to the importance of

technology in the sector.

RISK FACTORS

In spite of these opportunities, Ukraine is not

a simple place to invest. Perhaps the most

obvious challenge is the civil conflict, centered

in the eastern provinces and Crimea. Notable

conflict began in 2014 when then President Viktor

Yanukovych, a pro-Russian supporter, refused to

sign an association agreement with the European

Union (EU). Opposition groups to the president,

called Euromaidans, supported closer relations

with the EU and ousted Yanukovych through a

series of violent protests. Russia used this as

justification to annex Crimea. The local Ukrainian

government in Crimea, along with Donetsk and

Luhansk provinces, was expunged and while the

conflict has since quieted, it is far from over (see

CHART 6).

This unrest is affecting Ukrainian farmers on

many different fronts. First, the majority of

provinces under Ukrainian government control

have lost access to Crimea and several eastern

provinces and vice versa. If you’ll recall from

the soil map earlier, these eastern and southern

provinces were among the richest in “black earth”

soil and therefore, some of the most productive.

Secondly, as a result of the conflict, farmers in

these affected regions have not only lost access

to the Ukrainian domestic market, but also

internationally, and are finding it increasingly

difficult to access inputs like fertilizer and

seeds. Before the conflict, Russia was a primary

importer of Ukrainian commodities, especially

from the eastern regions. Now, trade between

these regions has all but ceased, putting further

stress on Ukrainian producers. Finally, according

to Raimund Jehle, FAO’s regional coordinator for

Europe, many producers in these highly-fertile

regions have turned to household production

instead to survive the turmoil, and have given

up attempting to sell their products domestically

or abroad.19 Investors in Ukraine’s agricultural

sector need to carefully examine how their capital

may be affected by the ongoing civil conflict

before deployment.

The land moratorium currently in place, which

dates back to the transition from communism

to capitalism, is another barrier to entry. When

the Soviet policy of collectivism in Ukraine

failed in the late 1920s due to drought and snow

levels that resulted in the death of more than six

million Ukrainians, ancestors of the victims were

awarded small parcels of land averaging four

acres each. Then in 2001, Ukraine’s government

passed a law prohibiting the sale or purchase

of these plots, a moratorium that is still in

effect today over 25 years later and has been

extended nine times already.20 Productivity in

these 27 million hectares of distributed land is

severely lagging as there is no incentive for local

producers to improve land quality because they

don’t actually own the land. The moratorium also

prevents them from making any change to the

land’s designating purpose, so transformation to

a higher-value crop in the absence of selling it is

also not an option. Farmers are permitted to lease

their land for as long as 49 years, but since all

adjacent landowners would also have to agree to

lease in order to achieve any semblance of scale,

this is not a viable opportunity. Supporters of the

ban argue that without it, foreign companies from

the EU or the United States would flood into the

region, stripping this land away from generations

of Ukrainian farmers for pennies and providing

it to land developers. Calls for reform are getting

louder as Ukraine’s agricultural productivity continues to lag its neighboring countries.21 Many institutional investors will continue to

watch these policies closely, but until they

change for the better will likely keep their capital

on the sidelines.

Finally, a lack of transparency coupled with a

tendency by the government to emphasis short term solutions rather than pursue long-term fixes are additional risk factors to be considered.

According to the 2017 Corruption Perceptions

Index compiled by Transparency International,

Ukraine ranked 130 out of 180 countries, placing

it in the bottom third of all countries evaluated.

While they took their first steps to fight corporate

secrecy back in 2017 when they agreed to

share data on who ultimately controls Ukrainian

companies, past events such as former President

Yanukovych’s ability to syphon off at least US$350

million of Ukrainian public funds for his personal

benefit, will be challenging to overlook going

forward.22 Even Ukraine’s own Deputy Minister

of Agrarian Policy Olga Trofimtseva admits that

the decision to cancel refunds on export VAT for

soybeans and rape seeds was based on an “ad

hoc policy, when a policy is not based on some

strategy or long-term vision, but a short-term

reaction to changes.”23 Yet another indicator of

the government’s struggles to deal with systemic

issues is the fact that in the Ukrainian agricultural

economy, the investment burden is carried

primarily by producers financing production

from their own revenues. A study conducted by

UkrAgroConsult in 2017 showed that the share

of agricultural producers’ own money in total

investment volume reached 70 percent in 2016,24

indicating that this method of self-financing from

producers’ own profits is nearly exhausted. For

comparison, the next highest source of capital

investment came from bank credit and local

budgets at only 7.1 percent of total volume.

Continued civil conflict in some of Ukraine’s

most fertile regions, the 20-year-old-plus land

moratorium, and a lack of transparency and

financing opportunities for producers will

continue to plague Ukraine agricultural

producers as they search for alternate sources of

investment capital.

FUTURE OUTLOOK

Ukraine’s growth potential as a low-cost,

strategically-positioned grain producer is

an opportunity that must be approached

cautiously and with the right structure. Direct

farmland ownership, at this stage, is not an

option; and while long-term land leasing is

possible, it exposes investors unnecessarily to

naked commodity and legislative risks. While

an increasing number of experts believe that

opening up Ukraine’s land market to foreign

investors will not only solve the problem of

limited access to financing but also provide

incentive for foreign capital to come in, it is

not likely to happen in the foreseeable future.

Therefore, investors seeking to capitalize on

Ukraine’s projected growth in grain production

should seek debt-based investments into parts

of the ag value chain like transportation/storage

infrastructure, irrigation, and precision technology

applications. Finding and building a relationship

with trusted partners who have boots-on-the ground experience and a proven track record are essential for success. It also may be prudent

to consider co-investments with groups like the

World Bank or other NGOs as a way to bolster

credibility and further protect an investor’s

assets. While fortune does favor the bold, in

Ukraine, those first steps must be calculated and

protected, if one chooses to step at all.

SOURCES

1. Ministry of Economic Development and Trade of Ukraine. (2014). INVEST Ukraine Open for U. Retrieved from https://mfa. gov.ua/mediafiles/sites/rei/files/MEDT_ Brochure_A4_View.pdf, pg. 6

2. Latifundist.com, Top Lead. (201). 2016/2017 Ukrainian Agri Business Infographic. Retrieved from https://ukraineinvest.com/wp-content/uploads/2017/12/theinfographics-report-ukrainian-agribusiness-

2017-eng.pdf, pg. 5.

3. Baker Tilly, Credit Agricole and AEQUO. “Agribusiness.” Your Investment Matters: Agribusiness. https://ukraineinvest.com. 2018. Web. 10 October 2018.

4. Ibid.

5. Makarevych, Myroslava. “Olga Trofimtseva Talks about Future of Agriculture in Ukraine.” https://destinations.com.ua/business/ trends-innovations/395-olga-trofimtsevatalks-about-future-of-agriculture-in ukraine, UA Destinations, 31 May 2018. Web. 8

October 2018.

6. Baker Tilly, Credit Agricole and AEQUO. “Agribusiness.” Your Investment Matters: Agribusiness.

7. Ibid.

9. Ibid.

10. Ibid.

11. Ibid.

12. Ministry of Economic Development and Trade of Ukraine. (2014). INVEST Ukraine Open for U. pg. 19

13. World Bank Group. August 2015. Shifting into Higher Gear: Recommendations for Improved Grain Logistics in Ukraine.

14. Baker Tilly, Credit Agricole and AEQUO. “Agribusiness.” Your Investment Matters: Agribusiness

15. Banga, Bhavya. “Global Precision Agriculture Market Anticipated to Reach $10.55 billion by 2025.” https://markets.businessinsider.com/

news/stocks/global-precision-agriculturemarket-anticipated-to-reach-10-55-billionby-2025-bis-research-report-1027473195, Markets Insider, 21 August 2018. Web. 14 October 2018.

16. Gaidai, Nick. “Hot Investment: Agribusiness in Ukraine?” http://whartonmagazine.com/blogs/hot-investment-agribusiness-inukraine/#sthash.sFhG83nv.InVF7Hxr.dpbs, Wharton Blog Network, 21 May 2018. Web. 11 October 2018.

17. Krasnikov, Denys. “How technology is changing Ukrainian agriculture for the better.” https://www.kyivpost.com/ technology/how-technology-is-changingukrainian-agriculture-for-better.html?cnreloaded=1, Kyiv Post, 28 June 2018. Web. 15 October 2018.

18. Belenkov, Artem. “Artem Belenkov about Ukrainian Agricultural Holdings.” https://smartfarming.ua/en-blog/rozvitokagtech-v-ukraini-skladno-ale-mozhlivo, SmartFarming, 11 July 2018. Web. 15 October

2018.

19. [Food and Agriculture Organization of the United Nations]. (16 October 2016). The future of agriculture in Ukraine. [Video File]. Retrieved from https://www.youtube.com/watch?v=fSQrAasTHNo.

20. Gomez, James M & Choursina, Kateryna. “Ukraine’s Ban on Selling Farmland Is Choking the Economy: Kiev keeps putting off land reforms, despite pressure from the IMF and investors.” https://www.bloomberg.

com/news/features/2018-01-02/ukraines-ban-on-selling-farmland-is-chokingthe-economy. Bloomberg Businessweek, 1 January 2018. Web. 11 October 2018.

21. Ibid.

22. Transparency International. “Ukraine Takes Important First Step Towards Ending Corporate Secrecy.” https://www.transparency.org/news/feature/ukraine_takes_important_first_step_towards_ending_corporate_secrecy, Transparency International, 1 June 2017. Web. 17 October2018.

23. Makarevych, Myroslava. “Olga Trofimtseva Talks about Future of Agriculture in Ukraine.” 31 May 2018. Web. 16 October 2018

24. UkrAgroConsult. “Amounts of investment in Ukraine’s agricultural sector.” http://www.blackseagrain.net/novosti/on-investmentin ukraine2019s-agriculture, UkrAgroConsult, 24 May 2017. Web. 9 October 2018.