Our most recent contributed content article for Global AgInvesting’s AgTech Intel Newsletter. A concise, to-the-point commentary piece on Variable Rate Technology (VRT), adoption challenges, and what the future may hold. Many thanks to George Varvarelis and the Augmenta team for co-authoring this article and continuing to lead innovation in the sector. If you’re in California for the World Ag Expo this week, stop by Building C, Booth 3830 to visit with the team.

By Michael DeSa of AGD Consulting and George Varvarelis of Augmenta

Imagine you’re at the county fair with your date, casually strolling the grounds, watching ring toss games and listening to the joyful screams from the kids on the ferris wheel. Inevitably, you stumble across the fortune tellers and palm readers. Some people are passionate professors of this craft, while others are strict non-believers. Most, however, are willing to try it out of sheer curiosity, so long as it’s not too expensive. The adoption of Variable Rate Technology (VRT) — an application allowing farmers to apply different rates of crop inputs at each location across their fields — appears to have evolved in a similar fashion; some being true believers, but most only willing to put their toes in the water. We’ll take a deeper dive into VR tech, the headwinds facing a more widespread adoption, and what the future may hold.

What Problem is VRT Trying to Solve?

One of the indisputable facts we’ve learned in the last 15 to 20 years is that field variability is a real thing. Every farmer’s field has different agronomic needs, weather patterns, and soil profiles. As a result of this field variability, most farmers suffer some form of loss due to underperforming crops and overspend in inputs. VRT describes any technology that enables producers to vary the rate of crop inputs using a combination of variable-rate (VR) control systems with applications equipment, to apply inputs at a precise time and/or location to achieve site-specific application rates. However, if VRT was designed to solve a problem most of us agree exists, why have adoption rates been so slow?

VRT Adoption – How Does it Compare?

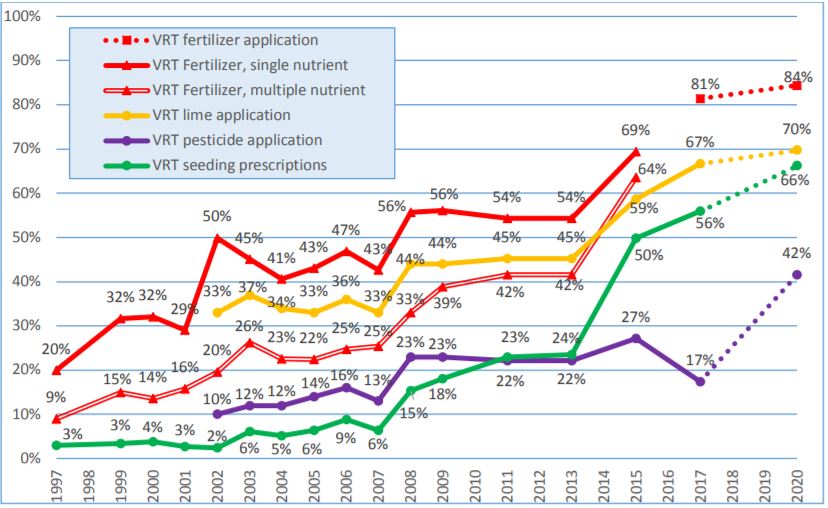

Like most things in agriculture, economic incentive and immediate need are two primary drivers for precision ag adoption, including VRT. By the end of 2017, for example, nearly 80 percent of U.S. ag retailers had adopted some form of GPS guidance[1]. Given that most U.S. farmers access new agtech through retailers, it’s safe to say guidance systems have been generally adopted by mechanized farmers worldwide. Why? Because the immediate benefits were very clear, the technology was easy to use, and the ROI was short and compelling. To the contrary, farmer up-take of VRT has been comparatively lower, rarely exceeding 20 percent anywhere in the world for cereals and oilseeds. These adoption rates indicate an “experimental” level of acceptance[2]. In spite of the widespread availability for VRT services indicated by Figure 1 and intense publicity and subsidies in some countries and states, VRT use by farmers has rarely broken this threshold.

Source: Erickson et al., 2018, CropLife-Purdue Survey

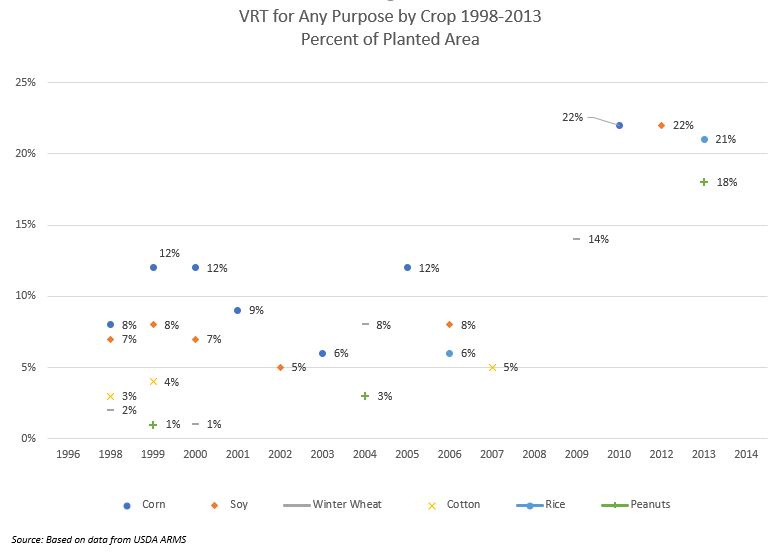

Figure 2 – VRT Adoption Purposes by Crop 1998- 2013

Challenges with Current VRT

Many of these headwinds to VRT adoption stem from the inadequacies of the technology and/or methodology used. First, ag retailers who offer Variable Rate Application (VRA) mapping generally do so as an add-on service to soil sampling. The problem with this methodology is that soil sampling data used to create VR prescription maps does not accurately consider nitrogen levels throughout the farm. In fact, nitrogen in nitrate form is evaporated by the time many of these samples reach the lab.

Drones and satellites are also commonly used today to create NDVI maps from which variable rate prescription maps are derived. NDVI maps tell a farmer how much more near-infrared light is reflected compared to visible red light. When translated into actionable data, it can provide insight into a variety of agronomic issues, but doesn’t specifically pinpoint why the crop is stressed (poor nutrition, disease, lack of water, or fertilizer, etc.). Further, the quality of the NDVI map is directly related to the sensor’s altitude and resolution. Logistics, high technical skills requirements, data transmission latency, and weather limitations all impact the use of drones/satellites for VR prescription mapping. While the use of VRT on tractors to enable mechanized input applications is a well-developed landscape, their effectiveness is still limited by the quality of the NDVI sensor.

Finally, many prescription maps today rely on a combination of soil samples (often taken only once per every acre or two) and drone/satellite NDVI imagery to create accurate enough maps in which to base agronomic decisions. With nitrogen fertilization windows being narrow and unpredictable, neither of these solutions allow the grower to capitalize on these maps in real-time.

What Must Change?

In order for VRT to break through the 20 percent adoption ceiling, it must make economic sense for the farmer. It must consistently illustrate that it helps increase yields and reduce input costs, ideally in the double-digit range. It must be easy-to-use and compatible with existing GPS systems. It must eliminate the high cost of site-specific information requirements (soil sampling) and developing individual prescription maps. The technology must be scalable and customizable to read more than one crop type without complicated configuration or retrofitting. Higher resolution, camera-based systems utilizing computer vision and machine learning are likely steps in the right direction. The solution must be able to be applied in real-time, and for commodity growers, grain prices may also need to improve before many will consider adoption.

Finally, the cost of being wrong must be cushioned by incentives for early adopters. Trial lease periods with free support, integration at grower co-ops and ag retailer levels first, and economic incentives from the downstream use of farmer data are just a few examples. In order for this to work, the bold must be rewarded by early fortune.

Michael DeSa is the founder/managing director of AGD Consulting, a U.S.-based, strategic advisory and business development firm servicing the agricultural and resource sectors in emerging and OECD markets. Services include farmland and agribusiness due diligence, project origination, market assessment, and competitive analysis for precision ag technology and international project management. DeSa can be reached at michael@desaconsultingllc.com.

George Varvarelis is the founder/CEO of Augmenta, a precision agriculture technology company. Varvarelis was a Ph.D. candidate in computer and embedded systems engineering while managing his family farms before deciding to put his engineering expertise into action to create scalable solutions for large-scale farming. Augmenta’s mission is to connect the dots of the global agriculture ecosystem and to augment the capacity of the arable land. Varvarelis can be reached at george@augmenta.ag.

[2] Professor Lowenberg-DeBoer, James. “Economic Considerations for Agricultural Big Data.” PowerPoint, Identifying Obstacles to Applying Big Data in Agriculture Conference, Houston, TX USA, August 20-21 2018.

Global AgInvesting‘s weekly GAI News recently announced its “Top 5 Stories for 2018”, of which the Brazilian piece we authored was the second-most read story last year! See the full list below:

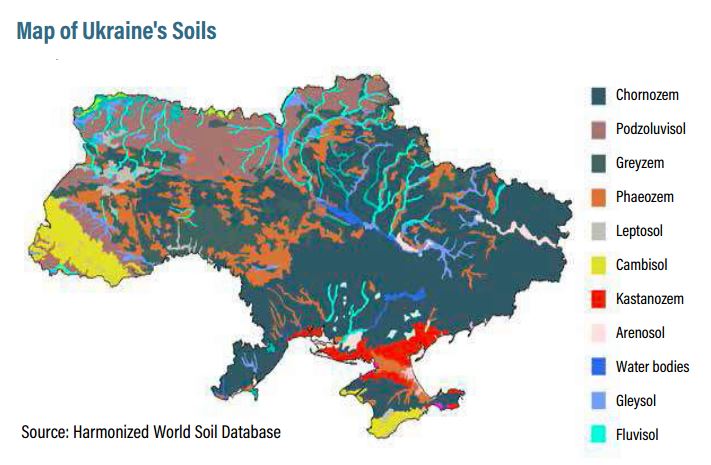

Ukraine’s agricultural production capability is often overshadowed by the country’s civil conflict and lack of business transparency. However, a closer look at this strategically-positioned agricultural powerhouse reveals there is ample opportunity for growth to meet the world’s increasing food requirements. Ukraine is the number two global leader in overall grain exports after the United States and takes the number three seat in corn exports.1 They are the number one producer of sunflower seeds and exporter of sunflower oil, reaching 1.16 billion tons of sunflower seeds produced in 2016/2017.2 Over 70 percent of the country’s total area is agricultural farmland, totaling more than 30 million hectares suitable for agricultural production.3 This level of production is accomplished on less than 10 percent of the total agricultural farmland in the United States, due in large part to the quality of soil. Ukraine boasts one of the richest concentrations of fertile soil on the planet, with over 30 percent of the world’s reserves of chornozem or “black earth” lying within its borders. The soil contains approximately seven to 15 percent organic matter necessary for quality crop production compared to two to eight percent in other parts of the world.4

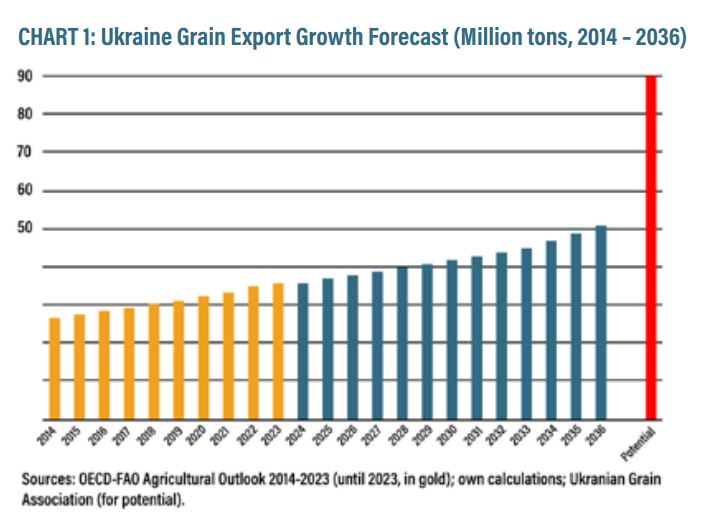

Even with quality soils and ample arable land, Ukraine is not producing anywhere near its potential. According to Ukraine’s Deputy Minister of Agrarian Policy and Food of Ukraine for European Integration, Olga Trofimtseva, the country harvested 66 million metric tons of grain in 2016 and 62 million in 2017.5 She believes this is far from the limit, commenting that Ukraine could easily harvest 100 million metric tons in the coming years, subject to the development and use of new technology and land reforms. She isn’t the only one who believes Ukraine is operating at a production deficit. The Organization for Economic Cooperation and Development Food and Agriculture Organization’s Agricultural Outlook for Ukraine projects Ukraine’s grain export potential could reach 90 million metric tons. Note that when the below graph was produced in 2014, Ukraine had already exceeded grain export projections for 2017 by nearly 20 million metric tons (see CHART 1).

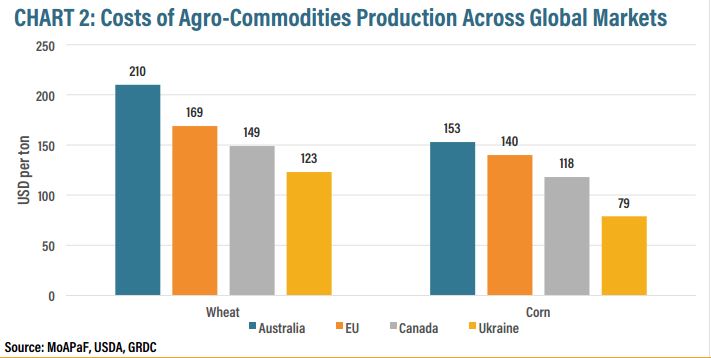

If Ukraine could reach these production levels, this would give them an exportable surplus of approximately 50-60 million metric tons, assuming 40-50 million for domestic consumptions.6 An exportable surplus is an indication of country’s ability to supply a lower cost product to the global market, thereby increasing their competitive advantage. The ability of growers to keep production costs low can have a significant impact on profitability and growth potential. A direct comparison of farmland prices in the Ukraine to other markets on a cost per hectare basis is inconclusive due to wide variations in farmland productivity and land prices, therefore, land cost per unit of production is a more meaningful comparison metric. The utilization of a production-based benchmark allows investors to compare land values using different production characteristics. The graph below shows costs of production for wheat and corn in the Ukraine compared to several other markets (see CHART 2).

Investing in farmland with low land costs per unit of production can allow an investor to realize greater capital gains through the application of things like new technology and modernized equipment, experienced management teams, and to the extent possible in the Ukraine, economies of scale. It is important to note, however, that this metric does not take into account the logistical costs/considerations of getting the commodity from the farm gate to the marketplace.

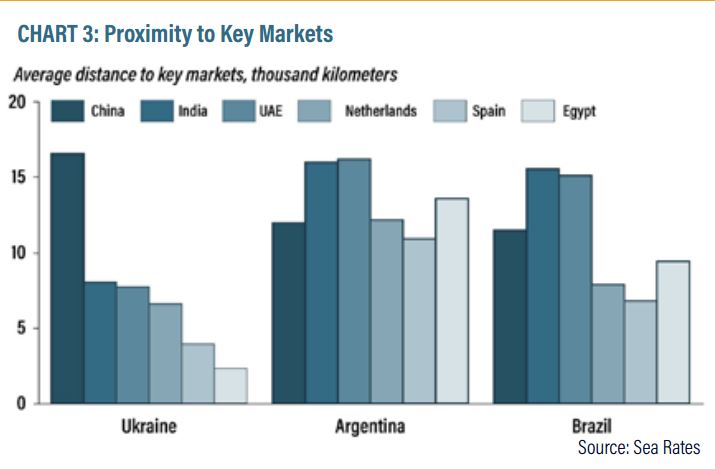

Ukraine’s geographic positioning to key European and Asian markets also provides additional cost-saving advantages. The graph below shows Ukraine’s advantageous positioning to key export markets (see CHART 3).

Proximity to these markets helps keep transportation costs low and also provides steady demand for commodities as middle classes in places like the EU and China continue to grow. Finally, a large labor pool – 25 percent of the Ukrainian population is employed in the agricultural sector7 – providing another supporting parameter for low-cost crop production.

High quality, naturally occurring soil – low-cost per unit of production as a result of strategic positioning to key markets and a large labor pool – are all positive indicators of Ukraine’s agricultural investment potential. The caveat is that, because of the severe limitations to land ownership by foreign investors in the Ukraine, investors should examine opportunities outside direct farmland investments that still capitalize on the land’s productivity potential.

OPPORTUNITIES As grain production forecasts predict a sizable increase in output from Ukraine, investments will need to be made into the country’s transportation and storage infrastructure to support this increased supply. Logistic costs for moving grain from Ukrainian farms to the Black Sea ports are still approximately 40 percent higher than cost for comparable services in France and Germany, and 30 percent higher than costs in the United States.8 These high costs are often the result of poor logistics, specifically outdated railway transportation equipment, underutilization of river transport, and insufficient storage capacity leading to higher spoilage. As a result, farmers receive lower shares of the market prices and shoulder these logistical costs from their own balance sheets. These losses in annual revenue potential can range between US$600 million to US$1.6 billion.9

CATCHING THE TRAIN A review of the Ukraine railway system reveals that currently 60 percent of grain volume in the Ukraine is transported via rail. The country boasts the 13th largest railway network in the world and can easily absorb the increased production forecasts with proper infrastructure development and equipment improvements (see CHART 4)

For example, current rolling stock of Ukrzaliznytsia (UZ), the state-owned Ukrainian monopoly that controls the vast majority of railroad transportation in the country, is outdated and ill-equipped. A recent World Bank study estimated that a US$64 million investment in Ukraine’s railway infrastructure, including 8,500 grain hoppers, new wagons, and locomotives, could yield an Estimated Rate of Return (ERR) of 21 percent.10

While transportation from storage to port is primarily done by rail in the Ukraine, significant investment is also needed to improve river and barge infrastructure and deep water port facilities. Only five percent of exported grain is moved along Ukrainian rivers, representing a formidably untapped opportunity to transport bulk ag products reliably, efficiently, and at a low cost, especially along the Dnipro River. River transportation in the Ukraine is often less expensive and more environmentally efficient than railway transport, with unitary transportation costs of three to 8.9 USD per ton compared to 10.5 for rail and 16.4 for road.11 The same World Bank study estimated a US$580 million investment could yield a 21 percent ERR. This would include dredging the Dnipro River’s shallow bottom to accommodate larger ships and prevent freezing during peak production winter months, lock passages, bridges, and port storage infrastructure. This type of investment could also lead to a capacity increase of five to six million tons of grain annually by 2022 and a 30 percent reduction in costs associated with road damages by 2022.

Improvement to rail and river transportation infrastructure will allow Ukrainian producers to offer even lower cost per unit of production to offtakers, but grain storage is yet another key component of the value chain suitable for foreign investment. Sufficient and quality grain storage infrastructure will help Ukrainian farmers minimize loss and store grain longer. In 2014, Ukraine had a grain harvest of nearly 64 million metric tons, however, existing certified storage infrastructure allowed for immediate storage of only 45 to 65 percent.12 Many existing facilities are more than 50 years old while the complementary infrastructure supporting drying, loading/unloading, and testing operations are energy-intensive and employ little to no recent improvement from precision technology.13 According to the World Bank, a US$1.5 billion investment into 6.4 million metric tons of new elevator capacity could reduce grain loss by 15 percent per annum yield and return early investors a 24 percent ERR. Without appropriate investment, poor logistics will become a bottleneck to sector development rather than a vehicle of trade facilitation.

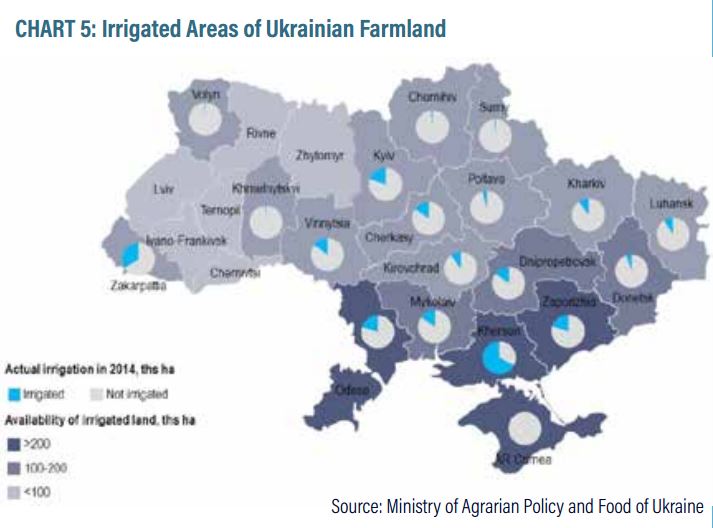

A Fluid Investment Opportunities exist in the upstream portion of the Ukrainian ag value chain as well, particularly in irrigation infrastructure. During the Soviet era, irrigation was widely used throughout the country. At one point, irrigation infrastructure grew by 100,000 hectares per year.14 While much of this machinery is now dated, proper maintenance and repurposing on the back of investment dollars could revitalize millions of hectares of existing infrastructure. At present, most Ukrainian farmers use dryland farming practices which place significant risk at the mercy of Mother Nature (see CHART 5).

Irrigated land has the potential to produce two to two-and-a-half times the yield compared to traditional dryland farming, without the risk of uncertain precipitation conditions. A recent State of Nebraska irrigation study showed a yield of 4.7 million tons per acre of corn on irrigated land compared to a yield of 1.8 million tons per acre on dryland, resulting in a revenue growth of over $240 more per irrigated acre. Under the right structure and management team, this could be a profitable way to participate in the forecasted Ukrainian agricultural uplift.

Adding Value with Agtech Finally, the application of precision technology to Ukraine’s agricultural sector will further allow producers to increase yield, reduce production costs, and optimize input consumption without the necessity for scale. There should be no doubt now that agtech is a booming sector across the globe. According to an August 2018 market intelligence report released by BIS Research, the global precision agriculture market is expected to raise US$10.55 billion by 2025, increasing at a CAGR of 13.7 percent from 2018 to 2025.15 With only three to four percent of arable land in the Ukraine under precision management, there is much room for growth.16 Early movers to this space who identify ways to apply precision technology to Ukrainian farm operations, while limiting their exposure to country risk, stand to do well.

One such area is soil erosion. According to the World Bank, Ukraine loses about 50,000 hectares of farmland every year from soil erosion and land degradation.17 Groups like AgriEye, a Ukrainian company founded in 2016, hope to cut this loss in half through the application of drone imagery, multispectral remote sensing, and open source geospatial imaging data. AgriEye uses this input data to create a precise field map of soil composition, which it then pairs with algorithms to analyze yield and provide prescriptive recommendations on how to irrigate and fertilize. While they charge for this service internationally, it’s free to Ukrainian farmers. Other Ukrainian firms like SmartFarming are applying data-driven solutions to help Ukrainian farmers reduce costs by as much as US$3,000 per hectare and save their producers more than 10 percent of inventories in a season through the re-equipment of machinery.18 Associations and accelerators like AgTech Ukraine, while only a few years old, are beginning to draw attention to the importance of technology in the sector.

Adding Value with Agtech Finally, the application of precision technology to Ukraine’s agricultural sector will further allow producers to increase yield, reduce production costs, and optimize input consumption without the necessity for scale. There should be no doubt now that agtech is a booming sector across the globe. According to an August 2018 market intelligence report released by BIS Research, the global precision agriculture market is expected to raise US$10.55 billion by 2025, increasing at a CAGR of 13.7 percent from 2018 to 2025.15 With only three to four percent of arable land in the Ukraine under precision management, there is much room for growth.16 Early movers to this space who identify ways to apply precision technology to Ukrainian farm operations, while limiting their exposure to country risk, stand to do well. One such area is soil erosion. According to the World Bank, Ukraine loses about 50,000 hectares of farmland every year from soil erosion and land degradation.17 Groups like AgriEye, a Ukrainian company founded in 2016, hope to cut this loss in half through the application of drone imagery, multispectral remote sensing, and open source geospatial imaging data. AgriEye uses this input data to create a precise field map of soil composition, which it then pairs with algorithms to analyze yield and provide prescriptive recommendations on how to irrigate and fertilize. While they charge for this service internationally, it’s free to Ukrainian farmers. Other Ukrainian firms like SmartFarming are applying data-driven solutions to help Ukrainian farmers reduce costs by as much as US$3,000 per hectare and save their producers more than 10 percent of inventories in a season through the re-equipment of machinery.18 Associations and accelerators like AgTech Ukraine, while only a few years old, are beginning to draw attention to the importance of technology in the sector.

RISK FACTORS In spite of these opportunities, Ukraine is not a simple place to invest. Perhaps the most obvious challenge is the civil conflict, centered in the eastern provinces and Crimea. Notable conflict began in 2014 when then President Viktor Yanukovych, a pro-Russian supporter, refused to sign an association agreement with the European Union (EU). Opposition groups to the president, called Euromaidans, supported closer relations with the EU and ousted Yanukovych through a series of violent protests. Russia used this as justification to annex Crimea. The local Ukrainian government in Crimea, along with Donetsk and Luhansk provinces, was expunged and while the conflict has since quieted, it is far from over (see CHART 6).

This unrest is affecting Ukrainian farmers on many different fronts. First, the majority of provinces under Ukrainian government control have lost access to Crimea and several eastern provinces and vice versa. If you’ll recall from the soil map earlier, these eastern and southern provinces were among the richest in “black earth” soil and therefore, some of the most productive. Secondly, as a result of the conflict, farmers in these affected regions have not only lost access to the Ukrainian domestic market, but also internationally, and are finding it increasingly difficult to access inputs like fertilizer and seeds. Before the conflict, Russia was a primary importer of Ukrainian commodities, especially from the eastern regions. Now, trade between these regions has all but ceased, putting further stress on Ukrainian producers. Finally, according to Raimund Jehle, FAO’s regional coordinator for Europe, many producers in these highly-fertile regions have turned to household production instead to survive the turmoil, and have given up attempting to sell their products domestically or abroad.19 Investors in Ukraine’s agricultural sector need to carefully examine how their capital may be affected by the ongoing civil conflict before deployment.

The land moratorium currently in place, which dates back to the transition from communism to capitalism, is another barrier to entry. When the Soviet policy of collectivism in Ukraine failed in the late 1920s due to drought and snow levels that resulted in the death of more than six million Ukrainians, ancestors of the victims were awarded small parcels of land averaging four acres each. Then in 2001, Ukraine’s government passed a law prohibiting the sale or purchase of these plots, a moratorium that is still in effect today over 25 years later and has been extended nine times already.20 Productivity in these 27 million hectares of distributed land is severely lagging as there is no incentive for local producers to improve land quality because they don’t actually own the land. The moratorium also prevents them from making any change to the land’s designating purpose, so transformation to a higher-value crop in the absence of selling it is also not an option. Farmers are permitted to lease their land for as long as 49 years, but since all adjacent landowners would also have to agree to lease in order to achieve any semblance of scale, this is not a viable opportunity. Supporters of the ban argue that without it, foreign companies from the EU or the United States would flood into the region, stripping this land away from generations of Ukrainian farmers for pennies and providing it to land developers. Calls for reform are getting louder as Ukraine’s agricultural productivity continues to lag its neighboring countries.21 Many institutional investors will continue to watch these policies closely, but until they change for the better will likely keep their capital on the sidelines.

Finally, a lack of transparency coupled with a tendency by the government to emphasis short term solutions rather than pursue long-term fixes are additional risk factors to be considered. According to the 2017 Corruption Perceptions Index compiled by Transparency International, Ukraine ranked 130 out of 180 countries, placing it in the bottom third of all countries evaluated. While they took their first steps to fight corporate secrecy back in 2017 when they agreed to share data on who ultimately controls Ukrainian companies, past events such as former President Yanukovych’s ability to syphon off at least US$350 million of Ukrainian public funds for his personal benefit, will be challenging to overlook going forward.22 Even Ukraine’s own Deputy Minister of Agrarian Policy Olga Trofimtseva admits that the decision to cancel refunds on export VAT for soybeans and rape seeds was based on an “ad hoc policy, when a policy is not based on some strategy or long-term vision, but a short-term reaction to changes.”23 Yet another indicator of the government’s struggles to deal with systemic issues is the fact that in the Ukrainian agricultural economy, the investment burden is carried primarily by producers financing production from their own revenues. A study conducted by UkrAgroConsult in 2017 showed that the share of agricultural producers’ own money in total investment volume reached 70 percent in 2016,24 indicating that this method of self-financing from producers’ own profits is nearly exhausted. For comparison, the next highest source of capital investment came from bank credit and local budgets at only 7.1 percent of total volume. Continued civil conflict in some of Ukraine’s most fertile regions, the 20-year-old-plus land moratorium, and a lack of transparency and financing opportunities for producers will continue to plague Ukraine agricultural producers as they search for alternate sources of investment capital.

FUTURE OUTLOOK Ukraine’s growth potential as a low-cost, strategically-positioned grain producer is an opportunity that must be approached cautiously and with the right structure. Direct farmland ownership, at this stage, is not an option; and while long-term land leasing is possible, it exposes investors unnecessarily to naked commodity and legislative risks. While an increasing number of experts believe that opening up Ukraine’s land market to foreign investors will not only solve the problem of limited access to financing but also provide incentive for foreign capital to come in, it is not likely to happen in the foreseeable future. Therefore, investors seeking to capitalize on Ukraine’s projected growth in grain production should seek debt-based investments into parts of the ag value chain like transportation/storage infrastructure, irrigation, and precision technology applications. Finding and building a relationship with trusted partners who have boots-on-the ground experience and a proven track record are essential for success. It also may be prudent to consider co-investments with groups like the World Bank or other NGOs as a way to bolster credibility and further protect an investor’s assets. While fortune does favor the bold, in Ukraine, those first steps must be calculated and protected, if one chooses to step at all.

SOURCES 1. Ministry of Economic Development and Trade of Ukraine. (2014). INVEST Ukraine Open for U. Retrieved from https://mfa. gov.ua/mediafiles/sites/rei/files/MEDT_ Brochure_A4_View.pdf, pg. 6

2. Latifundist.com, Top Lead. (201). 2016/2017 Ukrainian Agri Business Infographic. Retrieved from https://ukraineinvest.com/wp-content/uploads/2017/12/theinfographics-report-ukrainian-agribusiness- 2017-eng.pdf, pg. 5.

3. Baker Tilly, Credit Agricole and AEQUO. “Agribusiness.” Your Investment Matters: Agribusiness. https://ukraineinvest.com. 2018. Web. 10 October 2018.

4. Ibid.

5. Makarevych, Myroslava. “Olga Trofimtseva Talks about Future of Agriculture in Ukraine.” https://destinations.com.ua/business/ trends-innovations/395-olga-trofimtsevatalks-about-future-of-agriculture-in ukraine, UA Destinations, 31 May 2018. Web. 8 October 2018.

6. Baker Tilly, Credit Agricole and AEQUO. “Agribusiness.” Your Investment Matters: Agribusiness.

7. Ibid.

9. Ibid.

10. Ibid.

11. Ibid.

12. Ministry of Economic Development and Trade of Ukraine. (2014). INVEST Ukraine Open for U. pg. 19

13. World Bank Group. August 2015. Shifting into Higher Gear: Recommendations for Improved Grain Logistics in Ukraine.

14. Baker Tilly, Credit Agricole and AEQUO. “Agribusiness.” Your Investment Matters: Agribusiness

15. Banga, Bhavya. “Global Precision Agriculture Market Anticipated to Reach $10.55 billion by 2025.” https://markets.businessinsider.com/ news/stocks/global-precision-agriculturemarket-anticipated-to-reach-10-55-billionby-2025-bis-research-report-1027473195, Markets Insider, 21 August 2018. Web. 14 October 2018.

16. Gaidai, Nick. “Hot Investment: Agribusiness in Ukraine?” http://whartonmagazine.com/blogs/hot-investment-agribusiness-inukraine/#sthash.sFhG83nv.InVF7Hxr.dpbs, Wharton Blog Network, 21 May 2018. Web. 11 October 2018.

17. Krasnikov, Denys. “How technology is changing Ukrainian agriculture for the better.” https://www.kyivpost.com/ technology/how-technology-is-changingukrainian-agriculture-for-better.html?cnreloaded=1, Kyiv Post, 28 June 2018. Web. 15 October 2018.

18. Belenkov, Artem. “Artem Belenkov about Ukrainian Agricultural Holdings.” https://smartfarming.ua/en-blog/rozvitokagtech-v-ukraini-skladno-ale-mozhlivo, SmartFarming, 11 July 2018. Web. 15 October 2018.

19. [Food and Agriculture Organization of the United Nations]. (16 October 2016). The future of agriculture in Ukraine. [Video File]. Retrieved from https://www.youtube.com/watch?v=fSQrAasTHNo.

20. Gomez, James M & Choursina, Kateryna. “Ukraine’s Ban on Selling Farmland Is Choking the Economy: Kiev keeps putting off land reforms, despite pressure from the IMF and investors.” https://www.bloomberg. com/news/features/2018-01-02/ukraines-ban-on-selling-farmland-is-chokingthe-economy. Bloomberg Businessweek, 1 January 2018. Web. 11 October 2018.

21. Ibid.

22. Transparency International. “Ukraine Takes Important First Step Towards Ending Corporate Secrecy.” https://www.transparency.org/news/feature/ukraine_takes_important_first_step_towards_ending_corporate_secrecy, Transparency International, 1 June 2017. Web. 17 October2018.

23. Makarevych, Myroslava. “Olga Trofimtseva Talks about Future of Agriculture in Ukraine.” 31 May 2018. Web. 16 October 2018

24. UkrAgroConsult. “Amounts of investment in Ukraine’s agricultural sector.” http://www.blackseagrain.net/novosti/on-investmentin ukraine2019s-agriculture, UkrAgroConsult, 24 May 2017. Web. 9 October 2018.

We were recently featured on Cigars and Sea Stories, a Podcast for Veterans who want to make a difference in the world. Enjoy as we talk about our current endeavors with AG DTours, my service in the Marine Corps, and our experiences traveling throughout the region.

The current wave of agricultural reforms in Argentina could help the country recapture the global beef market share it has lost in recent years, says Valoral consultant Roberto Viton in an interview with Agrimoney.

Viton sees a brighter future for Argentine beef since the election of Mauricio Macri in 2015. Still, the process will take significant time and effort (I recently talked about the need for patience in Argentina in a recent blog post. Bottom Line: it will take time to change many years of poor economic management, so patience is in order) among producers who are looking to first improve their margins before expanding their production. In the first half of the year, there was much greater retention of cattle by Argentine producers with the goal of building back their herds over time (This is an indication that the local farmer sees future value in cattle and therefore is willing to forgo the immediate revenue in order to build equity in their farms through larger herds. This is a good sign).

Recovering market share lost to neighboring countries like Brazil, Uruguay and Paraguay will take time in terms of volume, price and quality. At the same time, Argentina will have to regain the confidence of foreign investors and prove to them that “the reforms are truly hear to stay.”

In summary, “I would say that the history of cattle is a history of patience,” says Viton. (I couldn’t agree more).

Earlier this month, we talked about Uruguay’s trade dealings with China. Today, we’ll look at how Uruguay and Argentina have come to a consensus on how to approach future trade deals with China. My emphasis is in bold with my comments in italics

Macri said that his government understands Uruguay’s need to have access to other markets and to be open to the worlds’ second largest economy.

Argentine president Mauricio Macri promised his Uruguayan peer Tabare Vazquez to look into the draft of a Uruguay/China free trade deal, and expressed their deep concern about political events in Venezuela suggesting that under the current circumstances the Nicolas Maduro government cannot be considered a member of Mercosur (Things in Venezuela are not looking good. Drastic shortages of food, medicine, electricity and other necessities are causing small riots. Organized crime and extrajudicial police killings have given the country a frighteningly high rate of murder and violence. Runaway inflation means that from March 2015 to 2016 a basket of basic goods for a family of five became 524 % more expensive).

During a meeting on Monday midday at the Olivos presidential residence in Buenos Aires, Macri said that his government understands Uruguay´s need to have access to other markets and open to the world’s second largest economy.

“China is an option for Uruguay. With Vazquez we ratified the need to speed up this deal, in principle from inside Mercosur, but anyway I promised an open attitude and to look into what Uruguay is requesting”, said the Argentine leader. (Mercosur, which translated means Southern Common Market, was created in 1991 as a trade agreement aimed at providing free circulation of goods, services, and productive factors within member countries (Brazil, Paraguay, Venezuela, Uruguay, and Argentina) through the elimination of obstacles to regional trade).

“We understand that Uruguay produces food for ten times their population(A population of only three million people currently feeding 50 million) so it is only natural they should look for markets, but the ideal situation would have been for the issue to have been presented by Mercosur as a block, as we are doing with the European Union” emphasized Macri(Earlier this year, the EU Trade Commissioner and the Foreign Minister for Uruguay, who currently holds the rotating presidency of Mercosur, discussed the next steps in the negotiations on an EU-Mercosur trade agreement. The EU and Mercosur agreed to exchange market access offers specifying ways to increase mutual openness to each other’s goods and services, including access to public tenders. Those discussions also resulted in the adoption of a road map for talks during the rest of the year).

Vazquez underlined the very generous attitude of Macri and thanked Argentina for having such consideration.

“We coincided in advancing in a free trade agreement with China through Mercosur. But [we need to take] into account that Beijing came up with the possibility of such a deal six years ago and Mercosur did not reply, it would be positive that at the next Mercosur meeting we address the issue”, indicated Vazquez.

“In the meantime Uruguay will continue to explore the way to advance in a free trade project with China. We’ve already presented the road map for such a treaty and the extent planned. China has not replied yet but when they do, it will be shared with all Mercosur members”, he added.

Regarding Venezuela, both presidents agreed that under the current situation, “we are deeply concerned with the political problems, and we shared the opinion that under these circumstances they can’t be members of Mercosur. The Maduro administration must be condemned and disavowed by all American countries since there is no respect for human rights” (As another point of context, in May of this year, Uruguay prepared to pass the president-pro-tempore seat to Venezuela by the end of June. However, Argentina, Paraguay, and Brazil fiercely opposed this. Their arguments against Venezuela’s new role cited the country’s failure to follow the union’s rules as well as concerns about the government’s stance against its opposition).

Vazquez went further and said concern, regrettably, grows by the minute and “we are looking forward to a peaceful solution to the controversy, to dialogue between the Venezuelan government and the opposition. We also talked about the mediation from Pope Francis”.

Macri and Vazquez added that during the next Mercosur meeting whether to apply or not the democratic clause on Venezuela will be considered, since that is the correct place to consider such option.

“Uruguay will be attending the meeting and demand respect for peoples’ right to express their opinions and be respected. That is the essence of democracy and the direct participation of peoples”, added the Uruguayan leader.

Other issues considered by the presidents were drugs and crime, pollution in shared rivers and water ways, natural gas sales and the possibility of building another bridge across the River Uruguay that acts as a natural border between the neighboring countries.

Finally Vazquez, who never had a good relation or chemistry with the Kirchner couple, was most grateful with Macri and his hospitality. “I am profoundly grateful for his hospitality and friendship, with the Argentine president we have found ample paths of understanding”.

An excellent article about the need for patience with the unfolding political and economic situation in Argentina. My emphasis is in bold with my comments in italics

It’s been almost one year since President Mauricio Macri shocked the world by winning Argentina’s presidential elections, and the country is in a state of flux — hovering in an uncertainty characterized by hope, anxiety, fear and just a few whiffs of the dreaded stench of failure.

Besides displaying a shocking lack of political PR and taking on a few petty wastes of time, this government is doing most things within its power correctly to right the course of a vessel that seemed destined to crash. (This includes eliminating a parallel exchange rate from the previous administration, completing an oversubscribed bond sale, and eliminating export taxes on many agricultural commodities like corn and wheat).

Despite these positive steps, one sinister question looms: Has the Macri government managed to avert the looming economic crisis entirely, or is it merely kicking the can down the road? It’s scary, but Argentina is in uncharted territory. Rather than boom, the economy is in a prolonged recession that could be heading for an all too familiar outcome — bust.

Yet this time, the question really isn’t about economic fundamentals. The real variable threatening Macri isn’t economic at all — it is time.(To me, this says that many potential foreign investors recognize Macri’s attempts to repair some of the underlying fundamental economic issues facing the nation. I believe, based in part on the oversubscribed bond sale, that there are many more foreign investors waiting on the sidelines to see if a resilient Macri administration and patience from the international community can allow these economic changes to positively affect the foreign investment climate of Argentina) Time, that fickle mistress, is persistently stalking Macri’s administration and is not on his side. And Argentines aren’t exactly famous for patience.

Now that Argentina is back on the world stage, there seem to be no shortage of Argentina investment-themed symposiums, conferences, forums, delegations, road shows, panels, seminars, and other names they give to the indistinguishable gatherings of hundreds of white men in suits assembled in windowless spaces to watch powerpoints and exchange business cards over mediocre coffee and stale snacks. (While I don’t necessarily agree with all of the author’s points here, I appreciate both her sarcasm and perception, especially the part about windowless spaces and mediocre coffee).

In the past, representing Argentina at these business rituals meant repeating some variation of the tagline, “Argentina: it’s not so bad!” Now the conversation invariably veers first to new opportunity, but then quickly pivots to the question of Argentina — same old risk?

People love to say that “Argentina has a crisis every ten years.” A nice round number, except it is 2016 and the country’s last real crisis was in 2001 (no, the 2009 global downturn doesn’t count). The truth doesn’t follow simple formulas. (This saying may actually be more applicable to the US market with the collapse of the dot com bubble in the early 2000s, the Great Recession in 2008/2009, and the unstable economic times of today.)

To understand the situation, let’s think of economies like dinner plates, spinning atop sticks. Balance is essential.

A balanced, diverse economy leads to stability

A poorly balanced plate will wobble dangerously and even crash to the floor from external conditions. Take a look at Argentina’s neighbors. Chile was thought to be as stable as they come, but a sudden drop in world copper prices have caused the country to wobble. Brazil was the next big thing in biofuels, technology, renewables — you name it. But a plunge in oil prices spun out the endemic corruption and tipped that plate right over.

So what do spinning plates and susceptibility to external crises have to do with Argentina?

From a purely economic standpoint, Argentina is just about the most stable, well-balanced, solid plate there ever was.The economy and the geography are large and diverse (One of the few countries in the world with the ability to be completely self-sustaining, hosting an abundance of natural resources, an educated population, and of course, famed agricultural land covering nearly 55% of the country). Argentina was resilient through the global economic crisis of 2009. Sure, soy is important piece of the pie but even when soy prices took a nosedive in 2014, Argentina’s plate wobbled a bit but kept on spinning. The good news is that despite more than a decade of Kirchnerism, during which Cristina Fernández de Kirchner and her band of merry thieves administration carried out a heist worthy of its own Netflix series, the plate was somehow able to keep spinning.

Macri’s government has acknowledged systemic flaws and is leading the country to come to terms with uncomfortable and unpopular realities, such as that 30 percent of Argentines live in poverty. The administration has acknowledged persistently high inflation and taken painful steps to bring it down. It has dismantled the capital controls that created a de-facto dual currency system (RIP Blue Dollar), settled with the holdout creditors (aka “vulture funds”) and are setting clear rules for doing business (To further highlight the points I made earlier).

Aranguren’s sad face 🙁

Perhaps most laudable, the administration has forced the population to acknowledge that energy subsidies for both electricity and gas are unsustainable and has launched a clear plan for prices to rise to meet generation costs. It’s not easy being Energy Minister Aranguren, the public face of these unpopular hikes. The man basically looks like he needs a hug all the time.

Yet that analysis misses a fundamental point of Macri’s challenge: to succeed, he won’t just have to right a plethora of economic distortions and rise above a mire of tragicomic corruption, he must also change a culture (This will take time, patience, and resilience on Macri’s part, but I think it can be done).

If Argentina’s economy is a plate, its next crisis won’t be caused by an external shock that throws an overweight area off balance. Argentina’s next crash will be caused by its people, who run from one side of the plate to the other, like an emotionally charged herd. Call it passion, color, soul, whatever you want — but we in Argentina are opinionated, loud, and most importantly impatient.

And without political patience, Macri will fail.

The key test will come next year, when the midterm elections will serve as a de facto referendum on his policies, many of which while are unarguably necessary albeit damningly unpopular.

Macri’s real challenge is not only to convince the world that Argentina can change; rather, he must lead his own people through a painful recession and politically maneuver entrenched powerful interests to restore an attractive labor market and an unsubsidized energy matrix.

(image/finedininglovers.com)

There is no doubt he is dedicated, but the question looms as to whether it is possible to convince a country of fiery, passionate Argentinos to endure a recession without throwing a tantrum and inexplicably sprinting off the edge of the plate (It is easy to understand that Argentines are looking for quick evidence of progress, as I’m sure many Americans will on the heals of our US elections, but after over a decade of systematically taking apart the economy, it will take time to fix the country’s inflation and poverty problems).

An article from the China Daily about recent trade discussions between Uruguay and China and how these discussions are impacting neighboring countries in LatAm. My bold and comments in italics:

Chinese President Xi Jinping (R) shakes hands with his Uruguayan counterpart Tabare Vazquez during their talks at the Great Hall of the People in Beijing, capital of China, Oct 18, 2016. [Photo/Xinhua]

BEIJING — Chinese President Xi Jinping and his Uruguayan counterpart Tabare Vazquez on Tuesday agreed to establish a strategic partnership based on respect, equality and mutual benefit. (Vazquez also signed infrastructure investment and technical agreements that will pave the way for greater agricultural exports to China)

The two heads of state made the decision during talks in the Great Hall of the People in Beijing following a red-carpet welcome ceremony.

Xi urged China and the Latin American country to maintain high-level exchanges and enhance communication at all levels to promote mutual understanding and trust. (Uruguay’s bid for a free trade agreement, however, is not without controversy. Uruguay is one of the five full members of MERCOSUR, along with Argentina, Brazil, Paraguay, and Venezuela. Argentina’s President, Mauricio Macri, said on Oct 20th that any China-Uruguay free trade agreement negotiations should be conducted through MERCOSUR. According to the bloc’s rules, full member states cannot negotiate free trade agreements with non-members without consent of their MERCOSUR peers. Vazquez responded to Macri by saying that Argentina and Brazil have been pushing for more flexible rules that would allow members to negotiate bilateral trade agreements)

China appreciates Uruguayan support for the Belt and Road initiative, and hopes both sides will strengthen integration of development strategies to upgrade economic and trade ties, said Xi.

China is willing to encourage more investment in Uruguay, channelled toward infrastructure projects, Xi stressed, adding that the country is also looking forward to expanding cooperation in agriculture, clean energy, communications, mining, manufacturing and finance.

In addition, Xi called on both sides to promote people-to-people exchanges and lift ties in culture, education, science and technology, Antarctica, tourism as well as football sport.

As for global affairs, Xi said that China is ready to strengthen collaboration with Uruguay in climate change, economic governance, UN’s 2030 Agenda for Sustainable Development, peace-keeping and South-South cooperation.

On China-Latin America relations, Xi stressed that China is a strong supporter for Latin American stability, unity and development. China is ready to work with Latin American countries to forge a community of shared future.(The other side of this argument was articulated by Argentina and Brazil when they voiced that China was the major exception to their pro-trade rhetoric. Both governments are under pressure at home that a China-Uruguay free trade deal would exacerbate their manufacturing sectors, particularly that Chinese imports could outcompete their local products. For example, Brazil wants to negotiate a trade deal that makes it easier to export the higher-value goods it produces, such as aircraft, but is reluctant to allow more Chinese imports into its borders).

Echoing Xi’s remarks, Vazquez said that the establishment of a strategic partnership will begin a new chapter of Uruguay-China ties. Uruguay welcomes more Chinese investment in the country and is willing to negotiate a free trade agreement with China.

Uruguay supports the one-China policy and backs China’s reunification, according to Vazquez.

Speaking highly of China’s significant role in global affairs, Vazquez stressed that Uruguay was ready to work with China to push forward Latin America-China relations and enhance coordination on international and regional issues.

Macri and Vazquez met on Oct 24 in Buenos Aires to further discuss Uruguay’s potential deal with China. More on that shortly

Below is an article from WorldFolio about the growing agro-industry in Uruguay and how it’s driving their economy forward. My bold and comments in italics.

The Minister of Agriculture wants to see the nation of 3 million people produce food for as many as 50 million in the next 15 years. But as Uruguay continues to increase the quantity of exports and reach new markets, it aims to maintain the high quality for which its agricultural and meat products are renowned (I think this will be the biggest challenge for Uruguay in their efforts to meet this goal: scale accordingly while maintaining high quality standards; something they’re world-renowned for).

Financial experts have long been bullish over the state of Uruguay’s economy, praising the nation for developing a strong institutional framework that has helped it weather external shocks.

Last year the World Bank categorized Uruguay’s macroeconomic policy as “prudent,” though the global finance overseer expressed concerns over “relatively high” debt and an export system that is based largely on connections to other countries in the region ( It should be noted that Uruguay’s national debt decreased by nearly $500M USD from Q1 to Q2 2016. This connection with other countries in the region doesn’t have to be seen as a completely negative characteristic, especially since Uruguay is the world’s 4th and 6th largest exporter of rice and soybeans respectively. Their beef products also export to over 150 world markets, speaking to their reach beyond LatAm). With this in mind, officials in Uruguay have expressed a desire to widen the reach of its agriculture industry outside of its neighboring states.

“Uruguay is a country that in 2005 produced food for 9 million people, and we were a country of 3 million,” says Uruguay’s Minister of Agriculture Tabaré Aguerre. “Today we produce food for 28 million people, and we are still 3 million. My goal is to produce food for 50 million people in 15 years.” (That’s a 3x increase in food production in just 11 years. All they have to do to reach 50 million is double again in 15 years. I think this is absolutely feasible).

According to Mr. Aguerre, 55% of Uruguay’s industrial output is made up of agro-industries, along with 47% of all industrial sector jobs. The agriculture minister explained this relative leg-up on the competition was due in part to Uruguay’s place in the worldand a wide range of recent changes in Uruguay’s economy.

“In the same way that investment have increased, the rate of exportation has also increased from Uruguay. Uruguay tripled the value of its exports, not in volume, but rather in value. We are a country that exports close to $10 billion in goods and services, with 80% of those being goods. And inside of that 80%, 78% of the exports are agriculture or livestock or agro-industry,” Mr. Aguerre says.

“Uruguay has comparative natural advantages, but beyond these, we have developed intelligent competitive advantages by improving genetics, the production system, research […] the national seed certification program [or] the national quality fertilizer program.” (This tells me Uruguay is doing more than just resting on the laurels of their God-given agricultural land. They’re innovating and adapting; a sign that their success in agriculture will continue).

Originally made agriculture minister in 2010, Mr. Aguerre has made a career as an agronomist researching everything from rice cultivation to cattle breeding in Uruguay. He was recently reappointed to the role in 2015 by Uruguayan President Tabaré Vazquez.

“That is how we are taking advantage of the window of opportunity that the decade from 2005 to 2015 gave us. [It has been] a time of great structural transformation in the world, particularly in the world of food production.”

Mr. Aguerre also highlighted an accelerated process of economic convergence during that time period, when “the growth rate for developed countries [was] less than the growth rate for developing countries.” (Once this gap closes, maybe completely, many international investors will begin to realize the underutilized value of agricultural land in Uruguay and LatAm, writ large. When that happens, expect land prices in Uruguay to rise with a growing investor sentiment. Get in early while prices are still good).

Because of that, he said, “the gap between the two is continuing to close.”

Executives in Uruguay have also pointed to the agricultural industry as a source of advantages in the world of business and economics.

“A few years ago, after several attempts to identify which would be the economic sectors that would push Uruguay to development, it was reconfirmed that the agro-industry was an extremely important for the economy of this country. The sector is not seasonal, gives activity the whole year and also invigorates other complementary sectors such as transport, or retail,” says Gastón Scayola, Vice President of Frigorífico San Jacinto NIREA S.A., a meat producer and exporter located in Montevideo. (Uruguay’s predictable, year-round rainfall, geographic location above the world’s largest aquifer, the potential for two crops per year growing cycles, developed land rental market, and limited government intervention also characterizes the strength of Uruguay’s agro-business market).

Left: Tabaré Aguerre, Minister of Agriculture | Right: Álvaro Silberstein, General Manager, Paycueros-Sadesa

“We have a great responsibility in terms of employment and the sector is the answer for most of the growth in the last few years (An understanding of the nation’s responsibility to its people). Obviously other activities such as the financial sector and tourism are also key activities for Uruguay, but our livelihood is agriculture for the long-term bet. In a world where much food will be needed over the coming years, this area of South America is destined to produce more and better.” (The world’s population is expected to reach 9.7 billion people by 2050. That equates to about a 60% increase in food production. I believe Latin American agriculture is poised to not only support this growth trend, but profit from it.)

Frigorífico San Jacinto has billed itself as a producer of high-quality beef products. In September 2015, the company made its first shipment of naturally produced Uruguayan beef certified by the US Department of Agriculture as “Never Ever 3” grade. This marking denotes that the meat is free from antibiotics and growth hormones, a fact which has reportedly helped to consolidate Uruguay’s exports in a market where demand for naturally raised and processed meat is growing steadily.(This is especially true as the demand from US consumers for quality, grass-fed beef continues to rise, e.g. Verde Farms, who get a good portion of their beef from Uruguay).

Mr. Scayola has also lauded Uruguay as a hub of traceability, a system whereby animals are monitored via a microchip attached to their ear. These microchips tell agricultural experts the dates when the animals passed inspection, the place they came from and where they are going. (Uruguayan beef is 100% traceable, meaning every piece of meat from an animal can be traced to its originating farm).

He explains that only a country as small as Uruguay could maintain such a close eye on their cattle and adds that his company has been the recent benefactor of a US decision to allow ovine(sheep) meat on the bone to be exported from Uruguay.

“The United States enabled us [to export] boneless meat a few years ago and now [they] have just approved the entry of meat with bone, thanks to the separation of sheep and cattle in the fields,” he says.

“With regards to sheep, we [have] 30% market share. We are the leading company and the one that has been the most aggressive in developing new markets and producing premium meat. San Jacinto are the only US enabled sheep plant.”

“It means a lot to get into the United States. [We can] enter the US market and fight with Australia, but also, once the United States approves the original mechanism theme compartment, immediately there is a high probability that Canada and Mexico [will also start accepting our goods], and that process can also open Europe. So we have many fronts and the United States is the first step of many.” (They understand the importance of needing to reach beyond the markets in their immediate vicinity into the global stage).

Executives elsewhere in Uruguay also highlighted a need to make the nation a more lucrative player in international trade. Álvaro Silberstein, General Manager of Paycueros-Sadesa, a leather exporter based Paysandú in western Uruguay, says that the country must specifically focus on agro-industry productivity.

“We have always considered that Uruguay should grow by relying on its export sector,” Mr. Silberstein says.

Founded in 1948, Paycuwas created with a “vision” that would advance exportation. As a part Sadesa, one of the leading group of tanners in the world, the company specialized in high-quality leather production for some of the “most prestigious” companies around the globe.

Mr. Silberstein explains the factors behind the quality of the hides the company uses.

“Meat companies operating in Uruguay are the largest exporters. Many also sell in the local market but they are basically exporters. Therefore, they are very technologically up to date. That makes the extraction of hides very precise – all machining and no knife. The hides are removed very healthily and that is also very important for us,” Mr. Silberstein says.

“In addition, because of the type of pasture we have and the type of production that is done, hides do not suffer as much as in tropical areas, where problems can affect the value of the material. That makes Uruguayan and Argentinian hides a sought after commodity in the world.”

Today the company boasts offices on five continents and a global export network that spans from South America to Asia. (Again, a global reach)

“Our vocation is as an exporter. In the case of hides, Uruguay does not have a market of significant consumption, and therefore the strategy is to add value to domestic raw materials and export them to the world.

“This new situation of slower growth should be seen as a new opportunity to re-look at export markets, and how to create the conditions for growth based on those exports. We have the conditions to do so because we have raw materials that will continue to be demanded around the world, and the ability to convert and add value that may be appropriate for the country through exports.” (China is also a strong market for Uruguay’s sheep and beef products)

However, others have urged an element of caution in Uruguay’s long-term export strategy. According to a study by the Observatory of Economic Complexity, Uruguay’s annual exports amount to more than $9 billion, with agro-industry staples like bovine meat, rice and soybeans being the largest export earners. The main importers of these Uruguayan goods are neighboring Brazil and Argentina, along with the US and China.

Industry insider William Johnson says this dependency on importing nations makes keeping a wary eye on economic activity outside of Uruguay crucial. (Agreed, but not a limiting factor, especially if Uruguay can continue to build their quality leather and sheep-meat markets up to the current levels of their beef products).

“Our goal is to eventually get to a point where we are not only exporting [material], but we want to add value [too],” he adds.

“We are a services country and we have to be tied a bit to the forces that guide the world.

“When Argentina goes off the rails, we have to look to our side to Brazil. When Brazil goes off the rails, we have to look to our side to Argentina. And when both are off the rails, it’s when we suffer big problems. We can’t export so much and then let sales and production fall. Because we are such a small country it’s difficult to compete in the rest of the world without the support of Argentina and Brazil.”